-

Crude oil continues to take the stairs to new highs

-

Term structure tightens- Bonus time for the front-to-back crowd

-

Brent-WTI rises- More gains on the horizon as US production declines

-

Upside targets for crude oil in 2021

A commodity’s market structure provides clues about the path of least resistance of the price. I view commodity fundamentals as a jigsaw puzzle with many moving pieces. Term structure and location and quality spreads are puzzle pieces that can form a picture of supply and demand dynamics.

Term structure is the forward curve or the price differentials for delivery at different periods. Contango, or a deferred premium, tends to signal equilibrium or oversupply conditions. Backwardation, or a deferred discount, often points to tight supplies or a fundamental deficit. The crude oil market tends to swing from contango to backwardation during its price cycles.

A location spread is the price differential for delivering a commodity in one area of the world versus another. A quality spread reflects different grades, compositions, or forms, of the same commodity. The price differential between Brent North Sea crude oil and West Texas Intermediate crude oil, the two global pricing benchmarks, is a combination of a location and a quality spread in the petroleum market.

The United States Crude Oil Fund (USO) and the United States Brent Crude Oil Fund (BNO) are ETF products that track the two leading petroleum standards’ prices.

Crude oil continues to take the stairs to new highs

Since November 2, crude oil has been on a steep staircase to the upside.

Source: CQG

As the daily chart of February NYMEX futures highlights, the energy commodity rose from a low of $34.50 to its most recent high of $53.93 or 56.3% over the past eleven weeks.

Nearby futures settled last week at $52.36 but ended on a bearish note as the price fell on January 14.

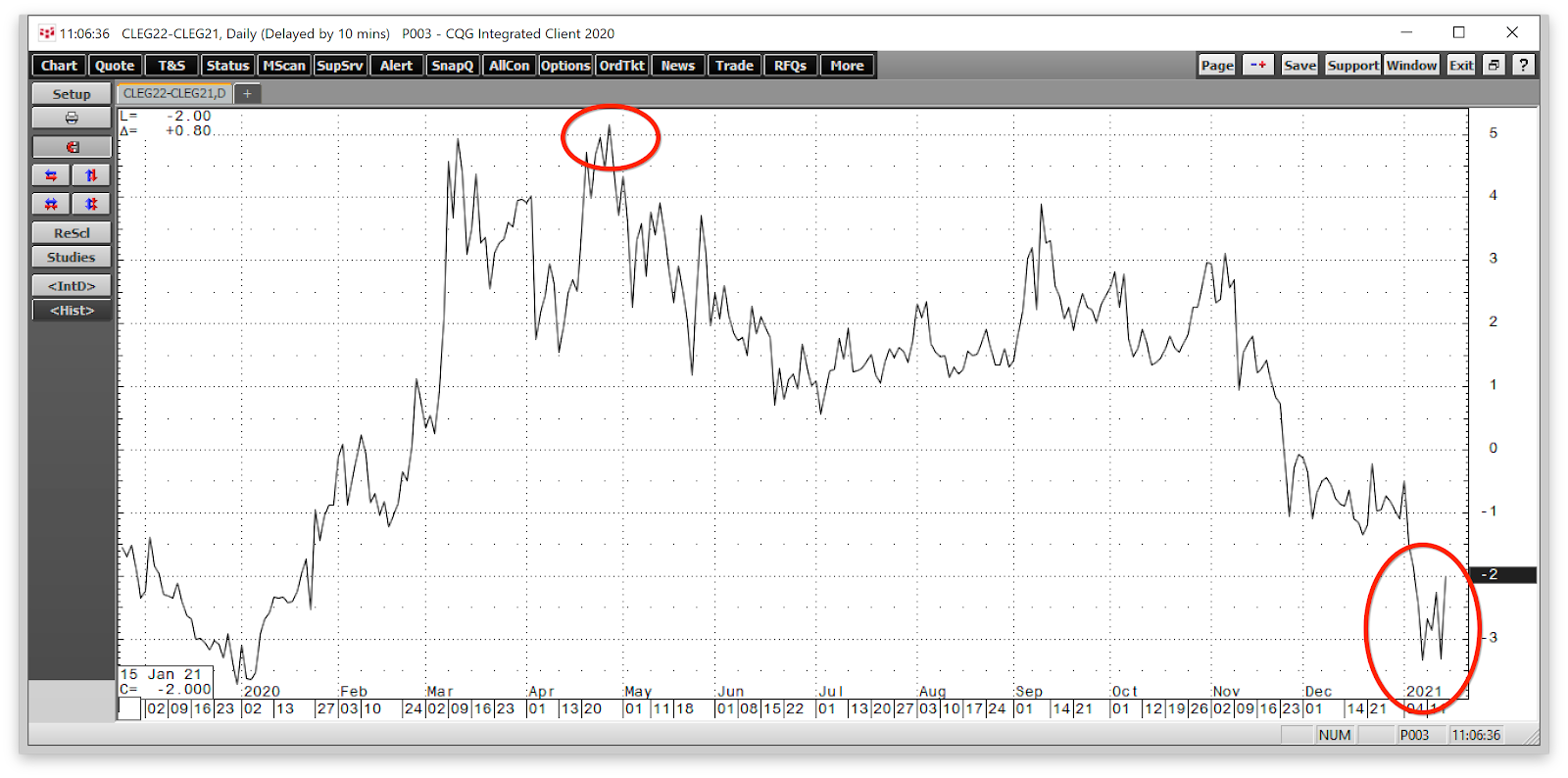

Term structure tightens- Bonus time for the front-to-back crowd

Term structure in the crude oil market flipped from the contango or a forward premium to backwardation or a deferred discount late last year.

The chart of WTI crude oil for delivery in February 2022 minus February 2021 shows that contango reached a high of $5.15 per barrel in late April 2020. The nearby contracts experienced a far higher level of contango or deferred premium as the May futures contract price fell below zero. The February 2021-February 2022 spread fell into backwardation in late November as the oil price moved higher. At the end of last week, it was trading at a $2.20 per barrel backwardation after reaching a low of $3.33 on January 8 and $3.32 on January 14.

The term structure displays tightness or supply concerns in the crude oil market. The move from contango to backwardation created substantial profits for the front-to-back crowd that bought nearby crude oil futures, took delivery, and stored the energy commodity when the contango reached wide levels in March and April 2020. At the same time, they sold crude oil futures for deferred delivery. The move into a backwardation creates the opportunity to unwind the spread by selling the oil in storage at a premium to the price required to close out the deferred short position.

Meanwhile, concerns that US production will decline under a far stricter regulatory environment under the Biden administration is causing the supply concerns that led to the current backwardation. The spread between the crude oil for delivery in February 2023 compared to February 2021 stood at $3.94 back as of January 15. Supply concerns have shifted the crude oil market’s term structure over the past months.

Brent-WTI rises- More gains on the horizon as US production declines

The price differential between Brent North Sea and West Texas Intermediate petroleum, the two benchmarks widened since late September. Brent is a seaborne crude oil that is the pricing benchmark for two-thirds of the world’s crude oil produced in Europe, Africa, and the Middle East. WTI is the American crude oil for delivery at a pipeline in Cushing, Oklahoma. WTI is the pricing standard for around one-third of the world’s petroleum. The different delivery points make the spread between the two a location spread.

When it comes to quality, Brent has a higher sulfur content than WTI, making it a preferable grade of the energy commodity for processing into distillate fuels like heating oil, diesel, and jet fuels. WTI is lighter and sweeter, making it the oil that is easier to refine into gasoline. The Brent-WTI is a location and a quality spread, but it is more. Since the Middle East can be politically turbulent, the spread also serves as a political risk spread for the energy commodity.

Source: CQG

The weekly chart shows that after reaching a 78 cents premium for Brent in late September, the discount for WTI moved to $2.72 at the end of last week. Over the past years, concerns about Middle East supplies caused the Brent premium to rise.

The recent surprise one million barrel per day production cut from Saudi Arabia pushed the spread to a higher Brent premium. Over the past decade, a rising Brent premium was typically bullish for the price of crude oil. In 2011 as the Arab Spring threatened Mid-East political stability, Brent rose to a $27.64 premium to WTI, and the price of nearby NYMEX crude oil futures rose to over $100 per barrel. Meanwhile, that dynamic could change in the coming months and years.

A dramatic shift in US energy production under the incoming administration could push US output lower, putting upward pressure on the price of WTI compared to Brent. Therefore, the crude oil price could move higher even if Brent moves to a discount to WTI over the coming months. Meanwhile, Iran remains a threat to peace in the Middle East. Any hostilities that impact production, refining, or logistical routes in the area that is home to half the world’s oil reserves could put upside pressure on nearby crude oil and the Brent premium over WTI.

Upside targets for crude oil in 2021

The technical targets on the upside stand at the February 2020 high of $54.50 and the January 2020 peak of $65.65 per barrel. The last time NYMEX crude oil futures traded over the $100 level was in 2014. On the way to the century mark, there would be technical resistance at the 2020 highs and $76.90, the peak from 2018.

Crude oil is a volatile commodity that takes the stairs higher during rallied and an elevator shaft to the downside during corrections, as we witnessed in April 2020. The energy commodity was on the staircase at the start of 2020.

The crude oil market could face an almost perfect bullish storm in 2021. Herd immunity to the coronavirus will increase energy demand, and the world continues to depend on fossil fuels. US output is likely to decline as energy policy shifts to a greener path. The value of the US dollar and all fiat currencies are trending lower under the weight of liquidity and stimulus causing the money supply to expand and deficits to rise. Inflationary pressures are building, which is bullish for all commodities, including crude oil.

At the beginning of 2021, two pieces of the crude oil market’s structure point to higher prices. The tightening trend in the term structure and a rising Brent premium have been bullish over the past decade. The path of least resistance of crude oil continues to be higher as of January 15. However, the risk of a correction will increase with the price of the energy commodity.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

5 WINNING Stocks Chart Patterns

7 Best ETFs for the NEXT Bull Market

The United States Oil Fund (USO) was trading at $35.83 per share on Tuesday morning, up $0.49 (+1.39%). Year-to-date, USO has gained 8.54%, versus a 0.96% rise in the benchmark S&P 500 index during the same period.

USO currently has an ETF Daily News SMART Grade of D (Sell), and is ranked #73 of 113 ETFs in the Commodity ETFs category.

About the Author: Andrew Hecht

Andy spent nearly 35 years on Wall Street and is a sought-after commodity and futures trader, an options expert and analyst. In addition to working with StockNews, he is a top ranked author on Seeking Alpha. Learn more about Andy’s background, along with links to his most recent articles. More…

Andy spent nearly 35 years on Wall Street and is a sought-after commodity and futures trader, an options expert and analyst. In addition to working with StockNews, he is a top ranked author on Seeking Alpha. Learn more about Andy’s background, along with links to his most recent articles. More…