Shares of edge cloud platform provider Fastly (NYSE:FSLY) are down 10.3% in the past two months. Fastly stock was down a massive 32.2% in October on the back of its lackluster third-quarter financial results. Many investors sensed a golden buying opportunity for the stock, criticized for being overvalued. However, when you dig into Fastly’s core business metrics, you realize that the company will continue on its elevated growth trajectory.

Edge cloud platforms are robust and provide a more efficient network architecture that minimizes hitches in performance. According to Grand View Research, the market will skyrocket to $43.4 billion by 2027, growing at a compound annual growth rate of 37.4%. 5G technology is expected to be a significant catalyst that is “expected to reorganize the industry architecture.”

However, growth isn’t a given, which is apparent with Fastly’s weaker-than-expected third-quarter results. Traffic slowed down due to the novel coronavirus pandemic and the ban on TikTok, representing roughly 12% of its revenue. Despite the weaknesses, the company has enough in the tank to weather the storm and return to winning ways.

A Weaker-Than-Expected Third Quarter

Fastly’s third-quarter results were marred by customer-specific challenges and business challenges created by the pandemic. Despite the tough conditions, its revenue rose 42% year-over-year to $71 million. However, analysts expected revenues of $73.57 million and a break-even quarter, where the company reported a loss of 4 cents per share. Additionally, the company’s enterprise customers held steady from the previous quarter accounting for 88% of revenue.

One of the significant hits to Fastly’s revenue is attributable to the loss of traffic from TikTok. TikTok withdrew its traffic, which accounted for 12% of Fastly’s revenue. The company will have to find a replacement for TikTok’s traffic in optimizing its load. Customer-specific traffic usage also dropped due to the Covid 19-led market slowdown. Despite this, the company acquired 100 new customers, including 11 new enterprise users. Moreover, average customer spend rose by a healthy 6% sequentially.

Another exciting development for Fastly is the acquisition of Signal Sciences, which offers an inimitable security architecture complimenting Fastly’s services. It provides substantial cross-sell and up-sell opportunities. Also, the company’s cutting-edge Compute@Edge technology is of limited availability. It is a server-less computing platform that is among the highest potential trends in the infrastructure space. It provides users with unmatched optimization, robust application performance and security.

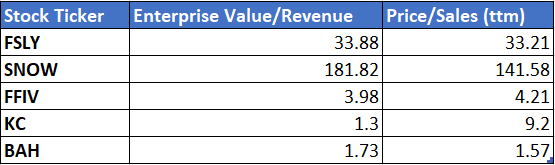

Valuation Is a Concern

Valuation has been a concern for Fastly’s investors, and rightly so. From the above table, we can see that the company’s valuation metrics are considerably higher than its peers. Barring Snowflake (NYSE:SNOW), its peers are significantly lower than Fastly in terms of the table’s two valuation metrics.

In the past three months, the consensus price targets for Fastly stock dropped considerably from $92.90 to $76.50. There is significant volatility in the stock’s price, with the massive discrepancy between high and low estimates. In the past three months, the stock’s daily price fluctuations exceeded that of 99% of S&P 500 firms.

Though it’s true that the stock is overvalued, I feel that there several reasons to justify its price. It has a few growth catalysts, including its Compute@Edge technology, to ensure it grows at a healthy pace. Even if the TikTok situation doesn’t get better, it continues to increase its customer base with every quarter.

Final Word on Fastly Stock

Fastly is facing some customer-specific challenges, but it continues to offset the dip in revenue by acquiring new customers. The company has a major growth catalyst in Compute@Edge up its sleeve, and its Signal Science acquisition should pay dividends soon.

Overvaluation remains a concern, but there’s enough reason to believe that the company can sustain its lofty growth for the foreseeable future.

Hence, you should invest in Fastly, especially after the recent dip.

On the date of publication, Muslim Farooque did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Muslim Farooque is a keen investor and an optimist at heart. A life-long gamer and tech enthusiast, he has a particular affinity for analyzing technology stocks. Muslim holds a bachelor’s of science degree in applied accounting from Oxford Brookes University.