American Airlines (NASDAQ:AAL) is still suffering greatly from the lack of travel by U.S. consumers. Since I last wrote about AAL stock on May 4, shares have fallen even more. Nothing has changed that makes me believe the stock has any chance of recovering soon.

In fact, I believe that there is more reason to believe that the company will likely have to reorganize. Sometime before the end of this year or early next year, American Airlines is going to need to reorder its balance sheet.

The bottom line is that equity shareholders are going to be severely squeezed. There may not be any further value in AAL stock. With that in mind, it makes sense to hold off on buying shares of American Airlines at the moment.

Crushing Debt Will Kill AAL Stock

In my May 4 article, I pointed out that the company has a crushing debt burden. Given its $6.7 billion cash burn during the second quarter and likely another $6 billion or more in Q3 and Q4 each, the debt will pile up.

For example, at the end of March, American Airlines had over $24.5 billion in interest-bearing debt. This does not include $15.7 billion in other current liabilities as well as $20.4 billion in other non-current liabilities. For example, it has a $6.1 pension liability on its balance sheet.

So if you add in another three quarters of cash burn, there will be at least $15 billion to $18 billion in additional debt or convertible equity. My guess is that most of this will be debt. That will take American Airlines up to over $40 billion in total debt.

As I pointed out in my previous article, you can’t run a company with negative free cash flow for very long. The interest on the debt, say at an average of 10%, is $4 billion a year alone.

That is over 4 times the net interest expense in 2019, when the company did not even make a profit. It also represents over twice the net income American Airlines generated in 2018.

So what is likely to happen is that note and bondholders will demand a large, if not the complete amount of a newly reorganized company. That would be the only way they would lower their total amount of debt or interest rates at American Airlines.

How to Measure American Airlines’ Revenue

For those investors that believe in the turnaround story with AAL stock, there is one very good real-time way to track the company’s revenue. This also applies to other airline stocks as well.

The Transportation Security Administration has begun a website related to the novel coronavirus that tracks the number of passengers going through screening checkpoints in U.S. airports. You can watch the daily checkpoint travel numbers here.

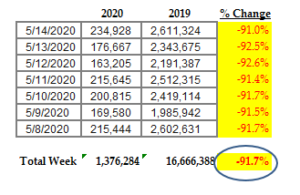

These numbers are nothing short of devastating. Moreover, there has been very little change in the month of May.

For example, in the past week ending May 15, the number of airline passengers is down 91.7% from last year. You can see this on the table I put together on the right.

Watch this site daily to see any kind of meaningful uptick by the end of Q2. Even if there is an uptick, it won’t necessarily be good news for AAL stock.

For one, the company has already discounted an uptick in airline travelers through the summer period. Management estimated that the cash burn would lower to $50 million per day by the end of June. This is expected to be down from $70 million on average for all of Q2.

Second, travelers are now facing even more obstacles, including long lines, mandatory face masks, enclosed space and virus outbreaks. But even more disconcerting is the prediction by the International Air Transport Association (IATA) that airline travel may not get to 2019 levels by 2024.

The Bottom Line

So far, there is little reason to believe that AAL stock will have any value by the end of 2020. A recent article from CNBC argues that while major airlines will survive, second-tier operators won’t be so lucky.

But that doesn’t necessarily mean the stocks of major airlines will survive. Investors should be extremely cautious with companies like American Airlines. AAL stock is simply not able to recover from the debt on its balance sheet.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here.