Wall Street looks vulnerable to another pullback here as the post-Covid-19 rebound capped out near a 50% retracement of the initial selloff and has been sliding sideways for weeks. To be sure, there are plenty of things to be worried about: Evidence of a prolonged economic shutdown, chaos in the energy markets, and concerns a quick fix for Covid-19 is not forthcoming. None of this has helped the energy stocks.

As a result, a number of dividend stocks look vulnerable here as a prolonged economic disruption increases the likelihood of payout cuts and further selling pressure.

Here are four I think investors should avoid at all costs:

Now let’s delve into exactly what makes each of these energy stocks a bad pick right now.

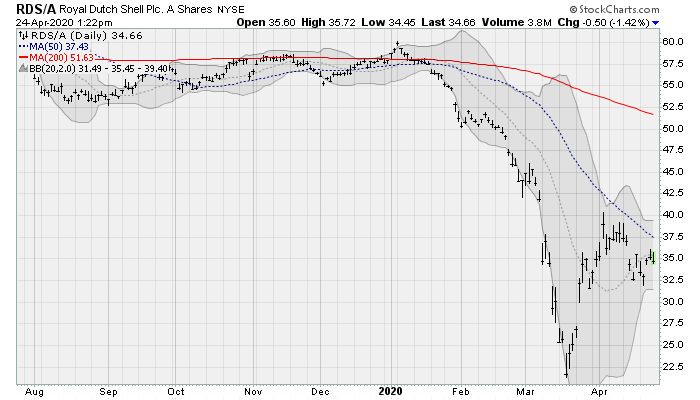

Dividend Energy Stocks at Risk: Royal Dutch Shell (RDS-A, RDS-B)

Shares of Royal Dutch Shell are languishing below their 50-day moving average, looking set for a retest of their mid-March lows as crude oil prices continue to suffer amid a global oversupply situation. Shares currently pay nearly an 11% dividend, but that doesn’t look likely to persist as wells are capped and production volume falls as storage tanks top off.

The company will next report results on April 30 before the bell. Analysts are looking for earnings of 56 cents per share on revenues of $55 billion. When the company last reported on Jan. 30, earnings of 74 cents per share missed estimates of 80 cents on a 19% drop in revenue.

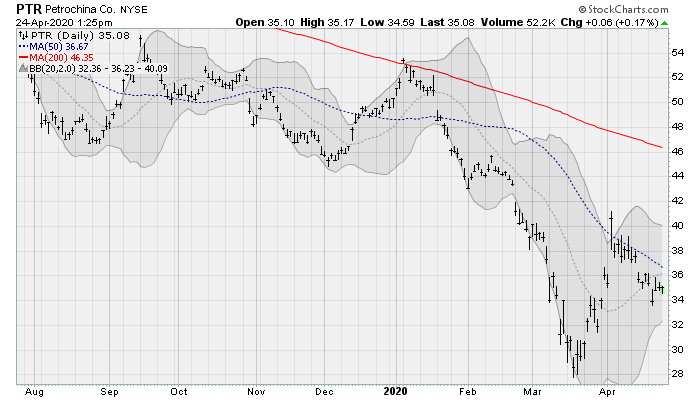

Petrochina (PTR)

Shares of Petrochina as also drifting lower after suffering a 35% decline from their early January high and capping a drop of nearly 60% from the highs set in late 2018. Shares were recently downgraded to “sell” by analysts at Citigroup. JPMorgan also recently downgraded to “neutral.” Currently, the stock pays a 6.7% dividend yield.

The company reported fiscal 2019 results in late March, with revenues rising 6% year-over-year. The company recently pulled its capital spending targets for the first time since 2015 amid a volatile and uncertain environment. Last year, the company spent nearly $42 billion, up 12.5% over the prior year.

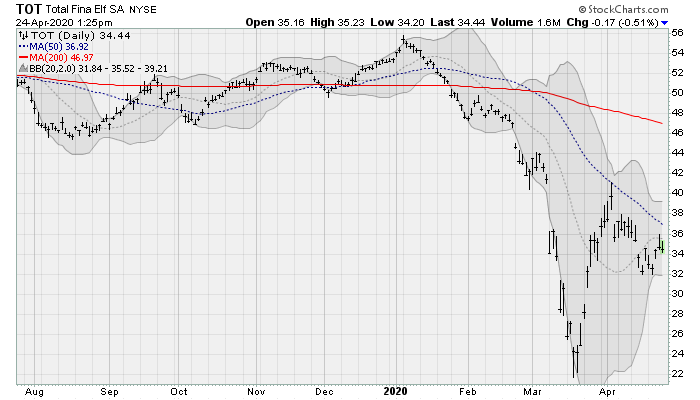

Total (TOT)

Total shares, which currently pay a dividend yield of 8.4%, are following a similar pattern to the others shown here, failing to retake its 50-day moving average. Cowen’s Jason Gabelman recently warned that Total along with BP had the highest exposure to probable production cuts — at roughly 8% vs. 4%. So, earnings could be very sensitive to top-line swings in output that could affect payout ratios.

Separately, the company along with Apache announced a significant oil discovery at its Sapakara West-1 well offshore Suriname, a project that is jointly owned. The project drills to a depth of 20,700 feet. Shares were recently downgraded to “neutral” by analysts at Morgan Stanley.

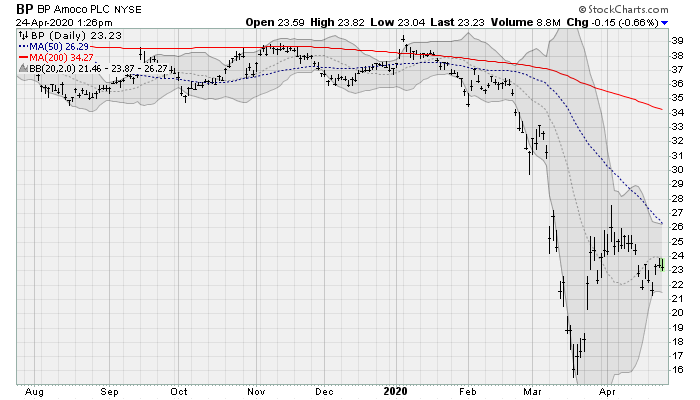

BP (BP)

BP shares, which pay a 10.8% dividend, are also currently below their 50-day moving average and look vulnerable to a return to the mid-March low which would be worth a loss of 30% from here. Not only is the company heavily exposed to production cuts, but the Wall Street Journal recently reported that the $5.6 billion sale of some of its assets to Hilcorp Energy is threatened by a drop in liquidity and fears over the health of the energy industry.

The company will next report results on April 28 before the bell. Analysts are looking for earnings of 25 cents per share on revenues of $79.6 billion. When the company last reported on Feb. 4, earnings of 13 cents per share beat estimates by three cents on a 6% drop in revenues from the prior year.

As of this writing, William Roth did not hold a position in any of the aforementioned securities.