Pinterest (NYSE:PINS) stock is doomed to slower growth and will likely continue losing money. These are the main reasons not to buy Pinterest stock. I could leave it at that, but my thesis requires some explanation.

To begin with, never be impressed with the lines that a major internet company spins about its terrible financial performance. No matter how the arts-and-crafts platform spins it, Pinterest lost money last quarter. And spin it, they do — let’s call it “How to Lose Money and Make It Look Like You Are Winning.”

Here is what I mean. It’s all about cash flow. Pinterest’s cash flow statement for Q3 shows that it lost $8.9 million in operating losses, and spent $20.4 million in capex. So its free cash flow was a loss of $29.3 million in the first nine months of 2019.

Pinterest stock is not going to rise anytime soon if the company keeps losing money like this. You can’t spin that. Pinterest tries to, saying it made $4 million in “adjusted EBITDA” during the quarter. But adjusted EBITDA can’t pay any bills and make PINS stock rise. Only free cash flow, which is cash flow after all major cash expenditures, including interest, taxes, capex and “adjustments.”

Now, to be fair, as of Q2, Pinterest had a free cash flow loss of $28.3 million. So that means its loss in Q3 was $1 million. That is significantly below the prior quarters, although still not positive.

Pinterest’s Growth Problems Keep Going

On the other hand, revenue growth is decelerating. That is, the once-rapid pace of its sales rise is slowing down.

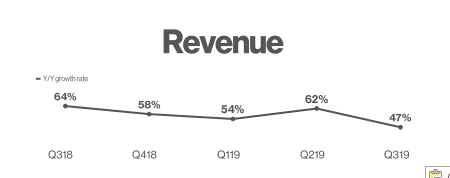

You can see in the chart to the right that revenue growth year-over-year started to slow this time last year.

In Q3 2018, revenue grew 64% Y/Y. But in the latest quarter, Pinterest’s revenue grew only 47% Y/Y. Some forecast revenue will only grow 36% Y/Y in Q4. That’s decelerating.

There are other issues related to this. For example, Pinterest makes the bulk of its ad sales revenue in the U.S. But U.S. monthly active user (“MAU”) growth is very low.

In Q3 U.S MAU grew just 2 million to 87 million. That represents growth of just 2.3% quarterly and 8% Y/Y.

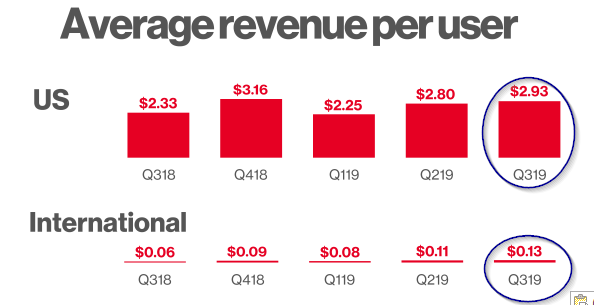

The problem is that the U.S. accounts for more than 95% of all of Pinterest’s ad revenue on an ARPU basis (Average Revenue Per User).

You can see this in the chart on the right. The U.S accounts for $2.93 per user, but international is just 13 cents per user. And remember most of the growth in Pinterest’s MAU is from international.

Not a Formula for a Fast-Growing Company

So growth in the U.S. is low and decelerating fast mainly from saturation. And the U.S. accounts for the bulk of Pinterest’s revenue. That is not a formula for a fast-growing company. In fact, the average global ARPU for Pinterest is just 90 cents. As I show below, this is well below Pinterest’s peers.

Another issue which analysts point out is that revenue is growing faster in the U.S. than its MAU base expands. That implies that Pinterest’s U.S. website is being ad-load saturated. In the end, users turn off to this kind of thing.

These issues lead to a suspicion that Pinterest stock is likely severely overvalued. So, let’s look at that.

Pinterest Stock Overvalued Compared to Peers

Pinterest stock trades at 9 times 2019 sales and about 6.7 times 2020 estimated sales. But this is the same valuation as Facebook (NASDAQ:FB), which is extremely profitable. For example, FB’s global ARPU is $7.26 per user.

Snap (NASDAQYSEAP is much more profitable on a user basis. SNAP’s ARPU is $2.12 vs. Pinterest’s 90 cents.

Furthermore SNAP has a smaller user base size than Pinterest. It measures this on a daily basis (DAU), rather than MAUs like Pinterest. SNAP has 212 million global DAU’s versus Pinterest’s 322 million MAU’s.

So even though SNAP generates 135% more revenue than Pinterest per user, it does so on a smaller base. One way to compare the valuations would be to assume the user bases were equal and then compare the price-to-sales ratios.

In that case, we would divide SNAP’s 11.6 P/S ratio by 1.35 x (i.e., multiply it by 74%) to find a normalized valuation for Pinterest. That equals 8.6 (i.e., 11.6 times 74%), but Pinterest trades for 9x 2019 sales.

The same is true for 2020 estimated sales. SNAP’s P/S ratio of 8.5 times 74% equals 6.29. But Pinterest’s 2020 ratio is 6.7. So in relation to both Facebook and SNAP, Pinterest stock is overvalued.

What Should Investors do with Pinterest Stock?

So, in summary, Pinterest is losing money on a cash flow basis. Its growth is decelerating and is too saturated with ads. Its U.S. MAU base growth is slowing and Pinterest stock is more expensive than its peers.

Maybe you should not buy-in to everything the company says about its glowing progress. It would be probably better to wait. At some point, Pinterest stock will trade at a bargain price. Better to buy it then.

Disclosure: As of this writing, the author did not hold a position in any of the aforementioned securities.