After an incredible run-up in the days after its initial public offering, volatility in Robinhood (NASDAQ:HOOD) is mostly absent. That did not stop the bearish selling on HOOD stock from accelerating after the company posted quarterly results on Oct. 26.

Robinhood fell after posting third-quarter results. What did investors not like?

Selling Pressures HOOD Stock

Robinhood posted net revenue growing by a modest 35% year over year to $365 million. Losses before income tax were a whopping $1.37 billion. This is up from a 2020 quarter three loss of just $11 million. The company recorded a share-based compensation expense of $1.24 billion.

On an adjusted EBITDA and non-GAAP basis, Robinhood lost $84 million. Investors who avoided the HOOD stock expected poor results. The app offers free trading but at a cost. When its relationship with Citadel came to light, user churn worsened.

Chief financial officer Jason Warnick said that churn was 870,000 accounts. This is still better on a percentage basis when compared to the first two quarters of 2021. To lower customer loss rates, Robinhood introduced extra services that will help the company win back customers.

Opportunity with Robinhood

Robinhood is building education content to help new investors become long-term investors. It rolled out education modules in-app in the last quarter. Since then, it added more tools and features. This will help customers have a better understanding of the market. More importantly, they will have a better familiarity with the Robinhood app. The more time they spend on the app, the more likely customers will deposit funds for investing.

Robinhood also started integrating Robinhood Snacks, the financial news content feeds, directly in its apps. In Q3, Snacks had over 23 million unique readers consuming the financial newsletter. Given its success, the company will continue supplying content, such as top financial news.

To speed up a new customer’s first investment, Robinhood started rolling out a new recommendation engine. Customers will get help on buying the first exchange-traded funds. The app will also stress the importance of diversification. The broader the customer’s portfolio gets, the less overall risk they have. Ideally, the total returns improve, encouraging investors to increase their portfolio size.

Risks of HOOD stock

Robinhood pioneered no-fee trading. It added $2.3 billion in net deposits in Q3, grew option revenue by 29% Y/Y to $164 million, and increased crypto revenue to $51 million, up 860% Y/Y. Competitors noticed those strong figures, forcing some of them to offer commission-free trading, too.

But Robinhood risks becoming a commoditized platform. It will need to increase its investments in content, customer support and app tools to differentiate itself.

The company launched 24/7 phone support. This may raise operating costs and hurt operating profits. Still, satisfied customers will spread the word to others. This will lower churn rates and reverse the exodus of customers after the Citadel controversy.

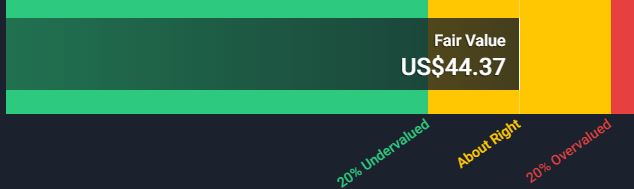

Fair Value

Based on a free cash flow to equity model, HOOD shares are worth around $44:

Click to Enlarge

The above fair value assumes a discount rate, or cost of equity, of 6.2%. The model assumes a perpetual growth rate of 2%. This is a reasonable value that is comparable to the government bond rate. Robinhood could earn a higher fair value if its customer growth accelerates. New investors with higher assets deposited would increase the company’s fees earned. This would raise its revenue growth rate and ultimately its fair value.

Growth Opportunity

Customers want to deposit, withdraw and trade cryptocurrencies. Robinhood is developing a crypto wallet that will let customers participate in the purchase of Bitcoin (CCC:BTC-USD) and Ethereum (CCC:ETH-USD).

Investors may think that platforms like Coinbase (NYSE:COIN) are competitors to Robinhood’s wallet offering. But the Securities and Exchange Commission’s questions on the unregistered securities are a bigger unknown to the wallet offers. Since Robinhood is a regulated entity, it is waiting for the SEC to offer more clarity on the crypto coins. As that happens, investors may accumulate shares of Robinhood to gain exposure to the crypto wallet segment.

Related Investments

Robinhood shareholders may bet on the company’s heavy investments in engineering and customer support will pay off in the end. To diversify from trading apps, investors may consider holding payment firms like Square (NYSE:SQ) and PayPal (NASDAQ:PYPL). Both firms offer strong growth in the electronic payments market.

Charles Schwab (NYSE:SCHW) is a bigger firm that markets value at a forward price-to-earnings of below 25 times. Schwab has a decades-long track record, too.

Your Takeaway

Robinhood is working hard to overcome the Citadel controversy, that led to higher customer churn at levels the company never faced before. As it strengthens customer support levels with 24/7 availability on the app, satisfaction levels will rise. Its unique tools, such as the recommendation engine, will also lift customer satisfaction. And I think those investments back in the business will eventually pay off.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Chris Lau is a contributing author for InvestorPlace.com and numerous other financial sites. Chris has over 20 years of investing experience in the stock market and runs the Do-It-Yourself Value Investing Marketplace on Seeking Alpha. He shares his stock picks so readers get original insight that helps improve investment returns.