The launch of Ford’s (NYSE:F) new F-150 pickup truck will meaningfully boost its revenue in the coming months, providing a catalyst for F stock. While Tesla (NASDAQ:TSLA) has provided information about its Cybertruck and compared it to the gas-powered F-150, the real competition between the vehicles has barely begun.

Ford’s electric F-150 will move the needle of its overall truck sales. Last year, Ford sold 900,000 F-150 pickups, bringing in over $40 billion of revenue.

Strategically, Ford’s failure to provide any details about the electric version of the F-150 is brilliant. Why should the company give its competitors like Nikola (NASDAQ:NKLA) or Tesla any information that would help them?

F Stock Is Set to Blast Higher

Ford’s announcement that it would bring the Mustang Mach-E to market raised consumers’ awareness of the company’s EV ambitions. The Mustang brand is already popular and successful. In the fourth quarter of 2019, before the coronavirus pandemic, sales of the Ford Mustang outpaced those of the Dodge Challenger and Chevy Camaro.

Ford sold 17,124 Mustangs in Q4 and 72,489 in 2019. Conversely,the company sold almost 900,000 F150s, making it much more important.

Ford is coy on the details of the F-150 EV, which is only in the prototype development phase. A prototype of the vehicle will not be produced until the start of next year.

In a statement, Ford said, “We have good inventory of the current model F-150 and we’re building at a higher-than-normal rate to ensure our stocks remain high to continue to meet customer demand.”

The sales of Ford’s current trucks will bring in enough revenue to offset the losses of its other divisions. But its continued underperformance in Europe and its high research and development spending, partly due to its development of EVs, will consume Ford’s cash flow.

Gas-Powered Trucks to Dominate

Ford’s EVs are in the early phases of development. Its Mustang Mach-E may end up looking significantly nicer than Tesla’s crossover SUV, the Model Y. And its F-150 EV may easily outsell the Cybertruck. But cheap oil prices will drive strong sales of gas-powered F-150s.

Despite trading in a steady uptrend since the market crashed in March and April, Ford is still undervalued. Its forward price-earnings ratio is around ten.

Speculators prefer to pay infinite valuations for EV stocks instead of buying Ford’s shares. But Ford’s EVs could be tremendously successful . And the company’s upcoming Bronco will trounce Fiat’s (NYSE:FCAU) Jeep.

Fair Value

Eight of the 12 analysts who cover Ford’s shares have a “hold” rating on the name. Their average price target on F stock is only around $7.00, according to Tipranks. Analysts rarely update their view on the firm because of its lack of positive near-term catalysts.

That is a mistake.

Sales of the Bronco could easily exceed the market’s expectations. If demand for it is very strong, Ford could decide to produce more trucks, off-road vehicles, and SUVs.

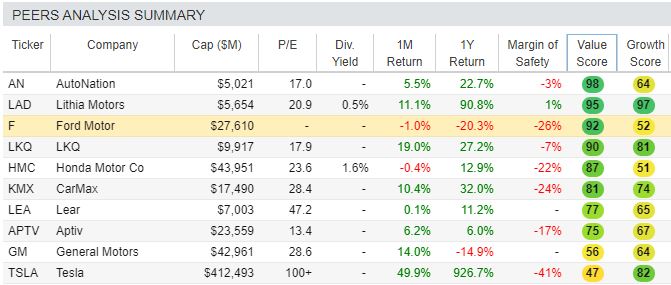

Table of value and growth score on F stock compared to Tesla

Chart courtesy of Stock Rover Research (click on the link for sample reports)

As shown in the chart above, Tesla deserves its high valuations because of its 82 out of 100 score on growth. Ford scores a 92 out of 100 on value and a disappointing 52 of 100 on growth. Despite my enthusiasm for Ford’s 2021 product lineup, the company has a poor history when it comes to increasing its profit.

The Bottom Line

Ford continues to disappoint its shareholders, due mostly to its continued poor operational execution. If it can control its costs and improve its product quality, it may have multiple successful products in 2021 with the Mustang Mach-E, the F-150 EV, and the Bronco.

Disclosure: On the date of publication, Chris Lau held a LONG position in F.