Recently, I gave my personal take on streaming when I purchased a Roku (NASDAQ:ROKU) device. Previously, I was tethered to the cord, always talking about the benefits of cutting it, but never truly understanding it. But with Roku, I wholeheartedly get why millions everywhere are abandoning traditional TV. With that, has my take on iQiyi (NASDAQ:IQ) and IQ stock changed?

Often billed as China’s Netflix (NASDAQ:NFLX), the investment concept of iQiyi stock appealed to those far smarter than me. These are the folks that saw the writing on the wall when it came to traditional TV. Following the implications to their logical conclusion, they cut the cord and joined the streaming revolution.

Indeed, buying a Roku device and enjoying previously unattainable benefits like on-demand content made me appreciate all streaming companies. I’m not just talking about IQ, but rather, the decision of big-name companies like Disney (NYSE:DIS) and AT&T (NYSE:T) to focus on content consolidation and streaming now made much more sense.

Clearly, streaming is the future, but will that future benefit IQ stock? Unfortunately, I have my doubts.

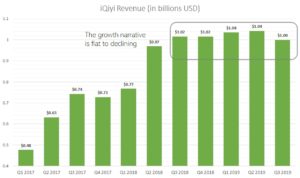

The company’s most recent earnings report for the third quarter didn’t help bolster confidence. Although IQ reported narrower-than-expected per-share profitability, it fell a bit short on revenue. Against a consensus target of $1.02 billion, the Chinese streaming giant instead rang up $1 billion flat.

That didn’t stop enthusiasm in iQiyi stock following the earnings disclosure. However, shares quickly came back down to earth over the next several sessions.

Worryingly, IQ stock dropped over 4% in the midweek session of Nov. 13. Rather than a discount, I see more volatility ahead.

IQ Stock Is Suffering an Identity Crisis

On paper, analysts consider Q3 as a mixed report: a beat on profitability expectations but a miss on revenue. But based on the technical performance of iQiyi stock, as well as the broader fundamental picture, I view the Q3 report as unambiguously disappointing.

Inarguably, IQ is a growth stock. The underlying company sacrifices positive net income in the here and now to invest in expansionary mechanisms. In terms of subscriber growth, management is achieving its goals, but in terms of sales growth, they’re flat to declining.

{kind=link}

It wasn’t just that Q3 2019 results produced revenue of $1 billion. Instead, over the last six quarters now, iQiyi has averaged revenue of $1.01 billion. And in Q3 2018, top-line sales came in just under $1.02 billion. As I said, the streaming firm’s sales trajectory is flat to declining.

Criticize Netflix all you want: the U.S.-based streaming company has consistently grown quarterly revenue over the last five years. And because of this historical consistency, Netflix has generated positive net income for several years.

But for IQ stock, a reasonable pathway to profitability is fading. Since at least 2015, net income has progressively sunk deeper into red ink. This year will continue this dubious trend unless we see a miraculous result in Q4.

And that won’t happen. In the most recent quarter, IQ’s net income was a loss of $516 million. In the year-ago quarter, it was a loss of $458 million. Clearly, the company is going the wrong way.

Ordinarily, for a growth stock, you’d comfort yourself with the growth narrative. But that’s also moving in the wrong direction for IQ stock. No matter where you turn, the fundamentals don’t make much sense.

China Is a Poor Market for iQiyi Stock

One of the other things I like about my Roku device is content options. From programming geared toward family viewing to NC-17 rated stuff, I control what I want to watch.

That’s the beauty of America and the western civilized world: we have the freedom to do how we please, so long as we don’t infringe upon other people’s rights. I believe we have the French to thank for this brilliant idea.

However, this mentality doesn’t fly in China. Internet censorship has long dogged attempts by American technology firms to break into the Chinese market. We’re talking huge brands like Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) and Facebook (NASDAQ:FB).

Supposedly, Chinese censorship is designed to protect pride in the mainland, which to some level I can understand. But it also devolves into the ridiculous, such as censorship of men wearing earrings.

And you know what? When it comes to entertainment, censorship stinks. It’s bad enough that IQ stock is having trouble with its underlying growth narrative. But to have a government-level headwind on top of it? This renders shares a speculative gamble rather than a sustainable investment.

As of this writing, Josh Enomoto is long AT&T.