Penn National Gaming (NASDAQ:PENN) stock benefited tremendously from the pandemic. But it hasn’t all been roses since then, judging by the current $100 hair cut it has suffered more recently. Still, in the long term, PENN stock should do well because it stands to benefit from several prevailing and sustainable trends.

Life is almost back to normal after the virus derailed our routines for almost two years. Yes, the use of masks is not likely to go away but at least hospitality businesses are back in business. Furthermore, sports are back on, so the betting business should starting gaining momentum soon.

Gaming in general is quick to recover because many people are drawn to it. Unless we suffer another surprise setback, the fundamental thesis for Penn is back on track. Before long, things will normalize and the company will be stronger. Management has proven its competency from having lived through the pandemic.

Unlike DraftKings (NASDAQ:DKNG) Penn lost its bid to operate in NY. But that’s just one setback of a huge addressable market potential. Besides, the company operates in 20 states and on several levels. Its partnership with Barstool Sports also widens its opportunity net.

Online gaming is exciting with more states legalizing it, but there is more to the PENN story than that. Penn National Gaming is huge in the regional gaming business. Losing out on one bid isn’t going to derail the company.

How to Approach PENN Stock Today

Case in point, despite the competition, sales grew 45% according to Penn’s February report. In addition, management seems efficient since they generated over $1 billion in cash from operations. Revenues last year were 60% larger than 2019, so it wasn’t a fluke. Other than 2020, they have carried a positive net income at least since 2015.

Value investors are not likely to squawk about its current metrics. The price-to-earnings ratio is 18x and the price-to-sales ratio is 1.23x. The harsh PENN stock correction brought those financials in line. Even if they don’t seem attractive, at least they won’t be a repellent either.

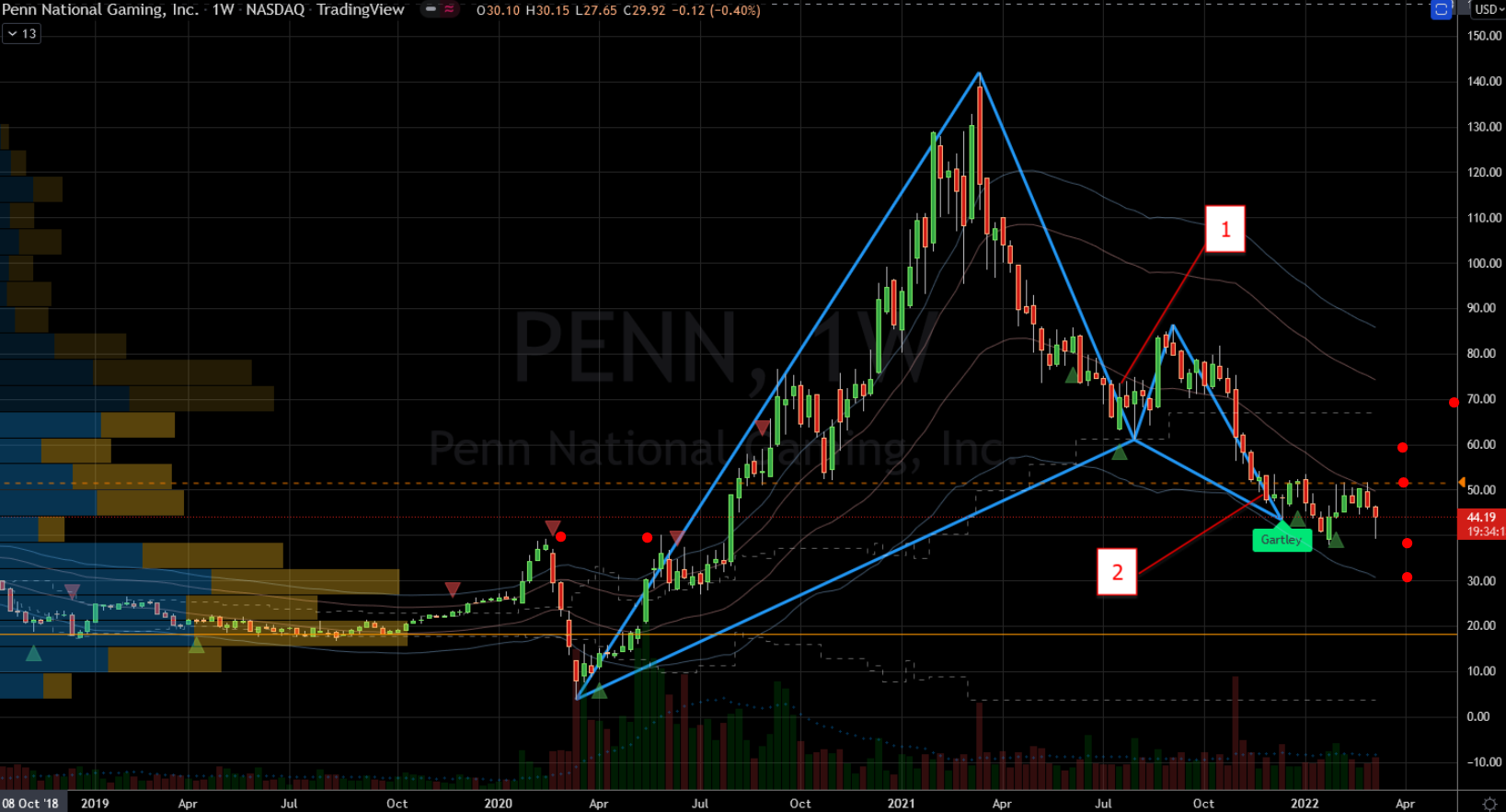

Technically there are signs of upside potential. When a stock hits a level and bounces off it twice, it could signify an interim bottom. The upside potential from this could extend 30% maybe even past $60 per share. But first the bulls will have to contend with a wall of resistance near $50 per share. Once they break through it, they can sling shot much higher to tackle the rest. Since this is a technical thesis, it would be best to set stop loss levels for safety.

While charts inspired this idea, fundamental investors can also adopt it. PENN stock is now hovering just above its pandemic breakout levels. Having lost 70% of its value, selling it much lower from here is tough. There are likely buyers lurking everywhere below current levels. If the markets in general stabilize, PENN is pretty close to a mid-term bottom. This makes today’s technical idea double as a mid-term swing investment too.

I’ve shared opinions on PENN before and my previous analyses fit perfectly with this one. In July of last year, prices were too high for comfort, so I raised a cautious flag. Back then I had “grave short term concerns” that panned out to be correct. But today, I am reiterating my more optimistic expectations. Today, PENN stock price is near the marker I called the “better base” last November.

On the date of publication, Nicolas Chahine did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.