Something big is going on here. As I’m writing this on Friday, Sept. 10, shares of installment-payment broker Affirm (NASDAQ:AFRM) are up 36% and AFRM stock is the number-one trending ticker on Yahoo Finance.

This undoubtedly caught many market participants off guard. After all, Affirm isn’t exactly a household name — but it could become one soon enough.

Of course, inking a deal with America’s (maybe the planet’s) biggest and most famous ecommerce business certainly won’t slow down Affirm’s forward momentum (more on that later).

Besides, estimate-topping fiscal results have a tendency to get market participants excited. So with a little bit of digging, we can identify what’s getting people so excited about Affirm — and at the same time, consider whether the buzz is warranted.

A Closer Look at AFRM Stock

Even though AFRM stock was pushing up against $125 on the afternoon of September 10, you might be surprised to learn that the stock’s gone higher than that.

Affirm shares actually reached a 52-week high of $146.90 on February 11 of this year. This might seem excessive, as there wasn’t any company-specific catalyst to justify that price move.

On the other hand, you likely recall that early 2021 was a time when Reddit-fueled short squeezes were in full effect. That phenomenon may have contributed to the earlier rally in AFRM stock.

Unfortunately, that surge didn’t last too long, as the stock fell below $50 in May. As for the most recent run-up, we’ll definitely delve into the likely causes of that.

Since the causes this go-around aren’t directly tied to social-media traders, we might witness a more sustainable price movement this time.

It wouldn’t surprise me at all if AFRM stock took out $200 within the next month or so.

A Win-Win Collaboration

Amazon (NASDAQ:AMZN) is a company that needs no introduction. It’s an ecommerce giant that basically destroys everything in its path.

Partnering in any way, shape or form with Amazon can quickly take a business to the next level.

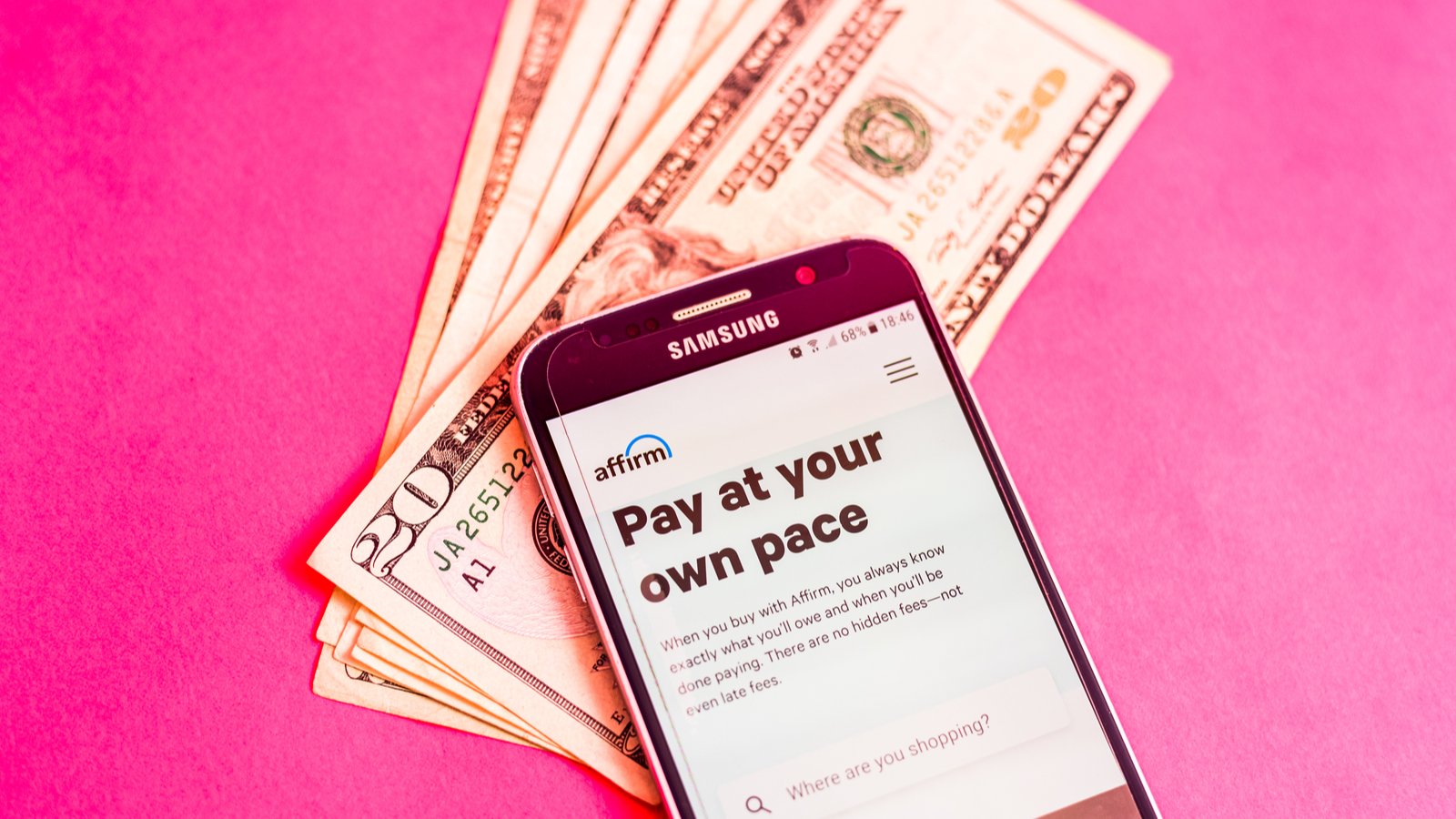

Therefore, it’s a major development for Affirm as the company announced that its payment solution will soon be available to Amazon’s online customers at checkout.

As InvestorPlace contributor William White explained, certain customers are already testing out this system, which allows them to split payments on purchases of $50 or more into monthly payments.

That’s part of the “buy now, pay later” paradigm America seems to be addicted to nowadays. I’m not sure if it will be good for consumers in the long run, but it’s certainly beneficial for Affirm.

At the very least, we can say that Affirm’s users won’t be charged any late or hidden fees. So, that’s a win-win for pretty much everybody involved.

Imperfect Results

Given the moonshot we’re seeing in AFRM stock, you might assume that Affirm is producing across-the-board positive fiscal results. Right?

Not quite. For 2021’s second quarter, Affirm reported an earnings loss of 48 cents per share. That’s worse than Wall Street’s estimate, which projected a loss of 29 cents per share.

But apparently, the investing community was willing to overlook that little detail. Instead, traders seemed to focus on Affirm’s quarterly revenues of $261.8 million, which outpaced Wall Street’s estimate of $226.39 million.

Or perhaps they were obsessing over Affirm’s first-quarter fiscal 2022 revenue guidance, which was put in a range of $240 million to $250 million. That range was higher than the prior estimate of $233.89 million.

The bulls can also cite Affirm’s 97% year-over-year growth in active consumers. So, all in all, there appear to be more positives than negatives to work with here.

The Bottom Line

There’s no guarantee that AFRM stock will reach $200 in the coming months, but we can’t dismiss the possibility.

This time around, the stock’s momentum is based on real data and an Amazon connection.

Which of these catalysts will propel the Affirm share price higher? Most likely, all of them will help the bull thesis come to fruition.

On the date of publication, David Moadel did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

David Moadel has provided compelling content – and crossed the occasional line – on behalf of Crush the Street, Market Realist, TalkMarkets, Finom Group, Benzinga, and (of course) InvestorPlace.com. He also serves as the chief analyst and market researcher for Portfolio Wealth Global and hosts the popular financial YouTube channel Looking at the Markets.