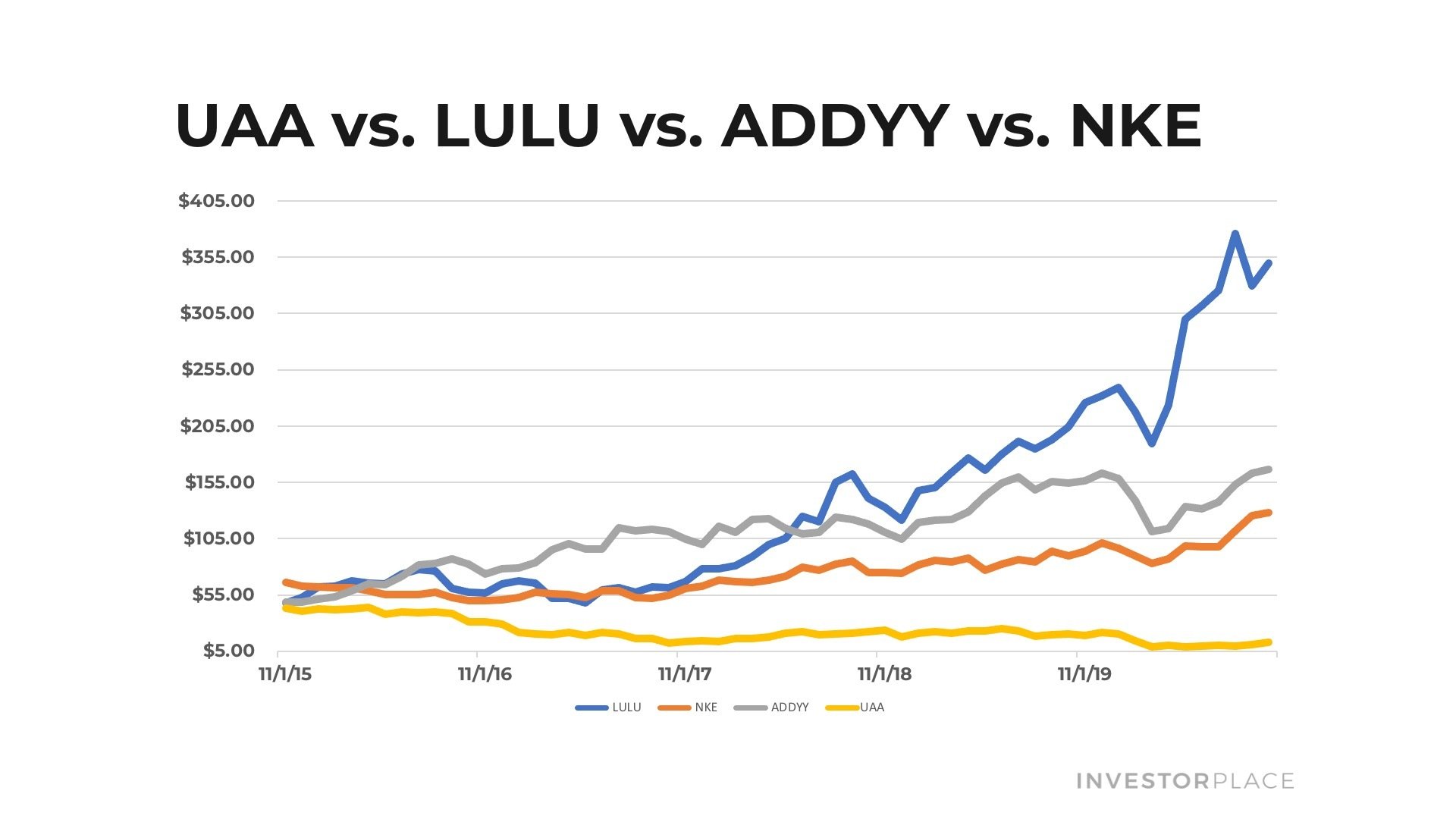

For years, Under Armour (NYSE:UAA) has been an eyesore in the otherwise burgeoning athletic apparel market, and Under Armour stock has paid the price. Over the past five years — while Nike (NYSE:NKE) stock has risen 100%, Adidas (OTCMKTS:ADDYY) stock has risen 300% and Lululemon (NASDAQ:LULU) stock has risen 600% — Under Amour has lost 75% of its stock’s value.

It’s an enormous discrepancy that can be explained by one thing: mismanagement of the Under Armour brand.

Specifically, management missed the athleisure wave in the mid-2010s, and in order to compensate for that, decided to aggressively expand product distribution through lower-priced channels in the late 2010s. All that did was dilute brand equity, and further dampen demand at a time when the brand’s star athletes — namely, NBA superstar Stephen Curry, NFL legend Tom Brady and golfing star Jordan Spieth — started to lose popularity towards the end of the decade.

That’s why Under Armour’s sales have risen a measly 13% over the past five years (which, in the athletic apparel market where Lululemon’s sales have doubled in the past five years, is nothing).

But, amid the Covid-19 pandemic of 2020, Under Armour management has taken huge steps in order fix its enormous branding problem. These steps lay the groundwork for Under Armour to bounce back in 2021, and for the company to finally participate in what has been an enormous athletic apparel demand boom.

As that happens, UAA stock could have a monster 2021 showing.

Under Armour Stock: What’s Going On?

For years, the athletic apparel space was on fire as consumers pivoted toward more broadly wearing comfy athletic shorts, leggings and tees in all lifestyle settings.

But, while the likes of Nike, Lululemon and Adidas reported huge growth quarter after huge growth quarter, Under Armour has not. Sales in 2019 rose 3%. They rose just 4% in 2018, and 3% in 2017.

That’s anemic growth for this industry.

What’s going on? Branding problems.

[embedded content]

Specifically, because Under Armour missed the boat on the athleisure trend in the mid-2010s, the company tried desperately to play catch-up in 2017, 2018 and 2019 by selling a ton of product into lower-priced channels, like Kohl’s (NYSE:KSS), on the idea that selling discounted product would increase brand reach.

It didn’t.

Instead, all it did was dilute brand equity, because when consumers started seeing Under Armour shorts and tanks pop-up in Kohl’s stores next to yesterday’s forgotten apparel brands, they started to affiliate Under Armour clothes with “cheap” and “uncool.”

At the same time, many of the brand’s star athletes lost popularity toward the end of the decade. NBA star Stephen Curry missed the entire 2019-20 NBA season. NFL legend Tom Brady left the New England Patriots, and is clearly no longer the best player in the NFL. Jordan Spieth — whose missed put in 2015 wiped millions off of Under Armour’s market cap — is hardly even talked about anymore (except for in reference to articles about how such a red-hot golfer slipped into anonymity so quickly).

All in all, the Under Armour brand simply lost all of its momentum. Consumers stopped buying UAA product. Demand globally fell off a cliff. And UAA stock plunged for years.

Fixing UAA’s Branding Problem

Amid the novel coronavirus pandemic, Under Armour is finally fixing its huge branding problem.

That is, the pandemic gave management the time to reassess the brand’s go-to market strategy, and they’ve come away with the right conclusion. In order for Under Armour to succeed in the long run, the company needs to improve brand equity, and stop selling so much product into off-price channels.

Throughout the second-quarter conference call, management talked about reducing brand exposure to the off-price channel. They are re-elevating brand equity by building out a more robust direct-to-consumer (DTC) sales channel, with premium product, at premium prices.

Those are the right moves to be making.

Getting UAA product out of Kohl’s and other off-price channels will help remove the negative stigmas that hamper Under Armour today. Building out a robust DTC channel will help Under Armour more strictly control, and thereby optimize, the shopping experience. Doing so will boost brand equity.

After all, Nike pivoted aggressively to DTC, too. Lululemon is entirely DTC. Both of those brands leveraged strong DTC experiences to cultivate powerful brand equity.

In order to facilitate this transition to premium and DTC, Under Armour is pushing a bunch of product into the off-price channel in the second half of 2020 to clear inventory. Of course, that will kill gross margins over the next few quarters. But it will also give Under Armour a clean slate to build a solid premium DTC business starting in 2021.

Plus, Stephen Curry is back for the the 2021 NBA season, his Warriors are fourth in betting odds to the win next year’s title, and he is reportedly getting his own clothing line at Under Armour (like the Jordan brand at Nike). At the same time, Under Armour recently launched a signature basketball shoe for another NBA star — Philadelphia 76er’s big man Joel Embiid — and this new shoe should provide a nice boost to 2021 sales.

In other words, Under Armour is taking all the right steps today to ensure that the company’s growth trajectory meaningfully improves over the next few years, and this improvement should start to show up in a big way in 2021.

Under Armour, Undervalued?

UAA stock is dirt cheap today because of the aforementioned branding problems.

But, if Under Armour can leverage a premium, DTC pivot and new, exciting products to fix those branding problems, then UAA stock today is too cheap for its own good.

That’s because management successfully pulling off this pivot will have two huge financial implications.

First, it will meaningfully accelerate revenue growth, from 3% to 4% today, to 5%-plus over the next few years. Second, it will meaningfully improve gross margins through a bigger mix of full-price sales and create visible runway for operating margins to scale to 10%.

If those two things happen – and I think they will – my modeling suggests that Under Armour will do about $1 in earnings per share by 2025.

Consumer discretionary stocks typically trade at 20-times forward earnings. Based on that multiple, a reasonable 2024 price target for UAA stock is $20. Discounted back by 8.5% per year, that implies a 2021 price target of nearly $16.

That’s about 25% above where share trade hands today.

Bottom Line on Under Armour Stock

For years, Under Armour has struggled with enormous branding problems.

In 2020, the company has taken significant steps to fix those branding problems.

In 2021, the company will start to realize the benefits of this enormous branding fix. Revenues will rebound meaningfully. Margins will expand. Profits will soar. So will the stock.

By the end of 2021, UAA stock will be closer to $20 than $10.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.

The New Daily 10X Stock Report: 98.7% Accuracy – Gains Up to 466.78%. InvestorPlace’s brand-new and highly controversial newsletter… is rocking the industry… delivering one breakthrough stock recommendation each and every trading day… delivered straight to your inbox. 98.7% Accuracy to Date – Gains Up to 466.78%. Now for a limited time… you can get in for just $19. Click here to find out how.