Artificial intelligence is set to be a massive trend in the coming decades. As such, investors are looking to find companies that can profit from the trend. But for several reasons, finding quality AI stocks is harder than it might seem.

First, some of the leaders in artificial intelligence are massive businesses, which means AI simply isn’t big enough. Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) and China’s Baidu (NASDAQ:BIDU), for instance, have invested heavily in artificial intelligence through both research and development spending and acquisitions. They qualify as legitimate AI stocks.

But what about, say, Microsoft (NASDAQ:MSFT)? Its Azure cloud platform offers machine learning, and AI is a feature of many other products. But the bulk of Microsoft’s business is based on more traditional software (and hardware) offerings. Given a $1.6 trillion market capitalization, it’s difficult to argue that AI, in and of itself, should or even could move MSFT stock higher.

The second issue is that individual artificial intelligence efforts themselves have vastly different importance. For Alphabet, AI efforts range from spending billions to develop fully autonomous driving to offering text suggestions in Gmail. Success (or failure) with self-driving cars can move GOOG stock. Gmail adoption simply doesn’t have the same effect.

Indeed, some form of artificial intelligence is a must for essentially every major company in the world. That doesn’t mean that they’re all AI plays. Most artificial intelligence efforts at this point qualify more as improvements on existing products rather than new lines of business.

So investors looking to play artificial intelligence need to make sure that they’re actually gaining exposure to the trend. These seven stocks often are thought of as AI stocks, but upon closer inspection for various reasons, they don’t actually qualify:

- IBM (NYSE:IBM)

- PROS Holdings (NYSE:PRO)

- Intel (NASDAQ:INTC)

- Ambarella (NASDAQ:AMBA)

- Remark Holdings (NASDAQ:MARK)

- Veritone (NASDAQ:VERI)

- Palantir Technologies (NYSE:PLTR)

AI Stocks With Too Much Hype: IBM (IBM)

As far as AI stocks go, IBM might have been the first. But it’s been far from the best.

Back in 1997, IBM first brought artificial intelligence into the mainstream. Its Deep Blue supercomputer beat the world champion at chess. IBM seemed poised to lead the AI revolution, which seemingly made IBM stock a sure bet.

For a time, it was. The stock soared in the late 1990s amid the dot-com boom (and then bubble). Over the 15 years after Deep Blue won, IBM stock gained 380%. The Nasdaq Composite rose just 120% over the same stretch.

In recent years, however, IBM stock has struggled. And its AI efforts are a reason why. The company’s Watson offerings haven’t been successful enough. IBM infamously saw revenue decline for 22 consecutive quarters. Legacy businesses like mainframes drove the decline, but AI growth disappointed as well.

As a result, IBM stock is headed in the wrong direction. Over the last eight years, it has lost 41% of its value. The Nasdaq has rallied 262%.

And it’s tough to see Watson and other AI efforts reversing that trend. Efforts to apply the technology to healthcare, in particular, haven’t worked out. Despite billions of dollars in investments and acquisitions, at least one former IBM employee has said that IBM no longer is “on the cutting edge.” Investors looking for AI stocks to buy probably should stick with those companies that are.

PROS Holdings (PRO)

PROS Holdings clearly belongs on any list of AI stocks, as it’s actually a direct provider of artificial intelligence solutions. Solutions provided by PROS help e-commerce companies price their goods, and airlines estimate customer demand — all in real time.

So for investors taking the long view, PRO stock does look intriguing. But there are two big concerns.

The first is that PROS is facing a significant amount of pressure from the novel coronavirus pandemic. Airlines are key customers, a key reason why the stock is down 44% so far this year. It will take some time for that industry to bounce back — and to stop seeing PROS products as a luxury amid a spate of cost-cutting.

The second concern is that PROS isn’t profitable. The pandemic isn’t solely to blame. The company lost money in 2019, even on an EBITDA (earnings before interest, taxes, depreciation and amortization) basis. That financial profile seems to cast doubt on the strength of the product offering.

That’s not a death knell for a company with a big long-term opportunity. But PROS isn’t a relatively new growth stock. It was founded in 1985.

The product offering and the opportunity both admittedly are intriguing. At some point, however, even the fastest-growing AI company needs to make money. PROS, so far, hasn’t proven that it can, and with customers struggling, PRO stock may not rally until it can do so.

Intel (INTC)

One place to look for AI plays is in the semiconductor sector. Artificial intelligence and machine learning will require ever-larger amounts of computing power. The chip companies that can deliver the processors behind that power stand to make substantial profits.

The problem for Intel stock, however, is that the company hasn’t shown that it can become one of the sector’s winners. Years of development delays left the company behind at the 10 nanometer node. It’s now struggling to get to 7nm, while rivals are heading to 3nm.

INTC stock admittedly is cheap after it plunged following Q2 earnings. But it was the disclosure of yet another delay that drove the plunge. Meanwhile, investors in AI stocks aren’t looking for “cheap.” They’re looking for growth. Intel is not going to provide that growth unless it can deliver the processors needed to power AI applications. Right now, that seems unlikely.

Ambarella (AMBA)

In the beginning of the year, Ambarella looked to position itself as an artificial intelligence play. The developer of semiconductors for video applications has been trying for years to pivot away from its reliance on GoPro (NASDAQ:GPRO). That relationship sent AMBA stock past $120 back in 2015, but has left the stock “dead money” in the five years since.

There is some reason for optimism. Ambarella spent over $300 million developing its architecture. A partnership with Amazon (NASDAQ:AMZN) allows developers to run machine learning applications on any device with an Ambarella SoC (system-on-a-chip). Ambarella’s experience with video processing makes it a potential winner from AI applications in security cameras and, eventually, autonomous vehicles.

But the move into AI is fraught with risk as well. Ambarella hardly has any of those markets to itself; competition will be fierce, particularly in AVs. Ambarella’s revenue had stagnated even before the pandemic, and GoPro is not the only reason why.

More broadly, so-called “pivots” in tech in recent years haven’t worked out well. Market leaders generally have too much capital, and too much freedom to aggressively invest that capital instead of focusing on short-term profits. Ambarella might be able to crack the code, but despite management’s claims, this seems like a “show me story” as far as its AI ambitions go.

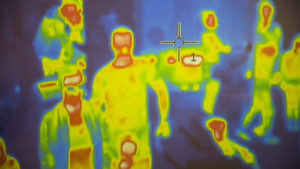

Remark Holdings (MARK)

Remark is another “show me” story, albeit one with a less-impressive past. The company has been trying to push its AI ambitions for some time, while also operating an online medical advice platform and an e-commerce business that sells bikinis.

The three businesses have had little success. In 2019, Remark generated revenue of $5 million, and an Adjusted EBITDA loss of nearly $27 million. Remark seemed to be on a path toward bankruptcy at the beginning of this year, and by April MARK stock traded below 50 cents.

But the pandemic gave the company an opportunity. Remark now offers AI-powered thermal imaging cameras to detect symptoms of Covid-19. The optimism toward that offering sent MARK stock soaring 600% in barely a month this spring. Remark took advantage of the spike to sell stock and fix its balance sheet, at least for the time being.

On this site in August, Luke Lango argued that the Covid-19 opportunity made MARK stock a potential winner, if admittedly a high-risk choice. I’m a bit more skeptical.

Remark hasn’t really delivered much in the way of major orders, with just $1.1 million in second quarter revenue attributed to the efforts. Research and development spending for the entire first half was just $2.1 million, which hardly seems like enough to develop a market-leading platform.

Given that Remark has a market capitalization of just $120 million, Lango is correct that the rewards if Remark succeeds are potentially huge. That seems like an enormous “if,” however.

Veritone (VERI)

Veritone has positioned itself as one of the leading AI stocks. The company claims that its aiWARE solution is “the world’s first operating system for artificial intelligence.”

It’s heady stuff. But the claims are belied by the company’s fundamentals. Growth has been meager, even before the pandemic. Surely, an AI OS would be a massive opportunity, yet research and development spending declined 43% year-over-year in the first six months of 2020.

Meanwhile, Veritone isn’t even predominantly an AI play yet. Less than a quarter of first-half sales came from aiWARE (a total of just $6.1 million); more than half came from its full-service advertising business.

It’s possible Veritone’s plans work out. But with VERI stock up 314% year-to-date on the back of AI optimism, they better.

Palantir Technologies (PLTR)

Investors waited for years for Palantir to go public. Now that it is, they don’t seem very enthused.

Palantir opened on the New York Stock Exchange at $10 on Sept. 30. It closed at $10 on Wednesday. In this market, the lack of an IPO “pop” should be a concern.

It probably is. Palantir has positioned itself as a “big data” company that focuses on the U.S. intelligence and law enforcement communities. Its software supposedly allows analysts, with the help of AI, to find patterns in the vast amounts of data collected.

But as New York magazine noted in an intriguing profile, Palantir’s offerings remain hugely labor-intensive. Part of that comes from the classic “garbage in, garbage out” problem: AI and machine learning aren’t effective if the data is inaccurate, as can often be the case. But whatever the cause, Palantir’s AI solutions aren’t quite the “magic bullet” observers believed they might be.

Indeed, Palantir’s fundamentals highlight the risk. Gross margins are below 70% — low for a software company. Operating loss last year was $576 million, more than 77% of revenue. (To be fair, margins improved substantially in the first half of this year.)

The risk to PLTR stock is that long-term margins aren’t going to be what its business model might suggest. Soft early trading in a market that has bid up the majority of IPOs suggest that plenty of investors see that risk as all too real.

On the date of publication, Vince Martin did not have (either directly or indirectly) any positions in the securities mentioned in this article.

After spending time at a retail brokerage, Vince Martin has covered the financial industry for close to a decade for InvestorPlace.com and other outlets.