When it comes to a selloff due to the coronavirus from China, one area that’s prime for bears has been the restaurant industry. But amid the historic fallout, it’s now a better time to look at restaurant stocks to buy and ready ‘to-go’ in your portfolio.

Thursday may not have elicited a full sigh of relief among investors. But a mild rise of just 0.47% in the S&P 500 and slightly spicy gain of 2.3% for the NASDAQ Composite was much better than the standard, stomach-churning fare of late. The price action also marked day one of a critical follow-through count for the broader averages, which have seen corrections of up to 32% over the last four weeks.

To say the least, the overall price action within the recently crowned bear market has been painful. Supply chain disruptions, forced closures, “shelter in” mandates and sensible “safe distancing” practices have been hard on most risk assets. But for restaurant stocks that have seen investors jumping through the windows and not simply running for the exits, the declines have been downright nauseating.

To be clear, the aggressive selloff in restaurant stocks hasn’t been entirely without good reason. The lost revenues will be in the hundreds of billions of dollars. Already, the National Restaurant Association is seeking a $145 billion recovery fund from the U.S. government. And it could get worse for restaurants if today’s closures and best practices are extended by authorities to become a longer new normal.

Still, there comes a time when investors should be smelling opportunity in restaurant stocks. And arguably, nibbling judiciously on the more extremely beaten down stocks already makes sense. That said, here are three “go-to” restaurant stocks to buy which will not only survive the coronavirus, but thrive in the weeks, months and years ahead.

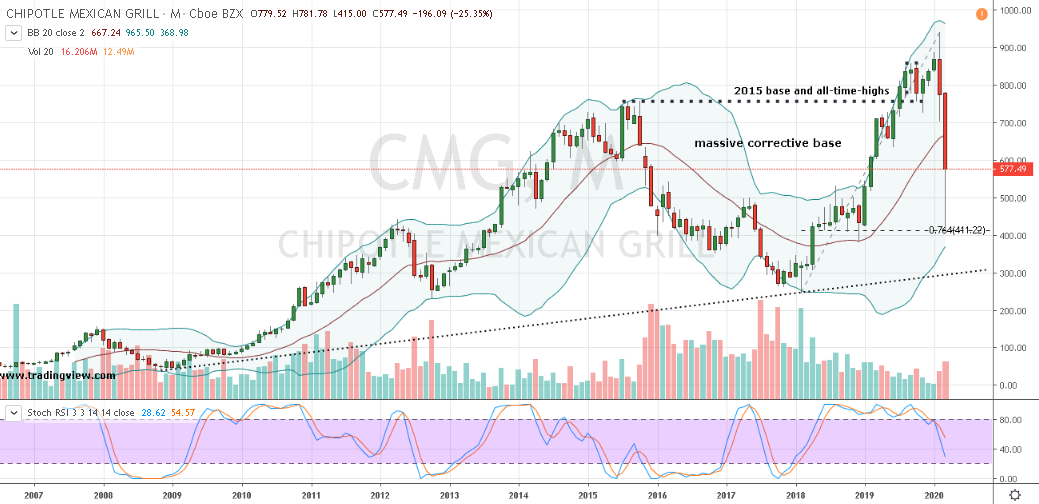

Restaurant Stocks to Buy: Chipotle (CMG

Click to Enlarge

Chipotle (NYSE:CMG) is the first of our restaurant stocks to buy. The fresh-fast burrito giant already maintained a loyal base of customers, and many of those also versed in the ease of ordering online for either in-store pick-up or delivery. Nothing has changed there.

Of course, dining in your local Chipotle is off-the-table. And earnings will undoubtedly take a hit in the short-term. Still, it’s also certain this restaurant stock’s online business will boom as folks like me continue to keep Chipotle in our lives and in our stomachs.

Technically, a 55% decline in share price that’s tested the 76% retracement level from CMG stock’s 2018 health-scare low is already being gobbled up by investors. I suspect with stochastics still pointing down, some digestion — or profit-taking — of those gains is in order. With that in mind, Chipotle is a restaurant stock to buy on a pullback.

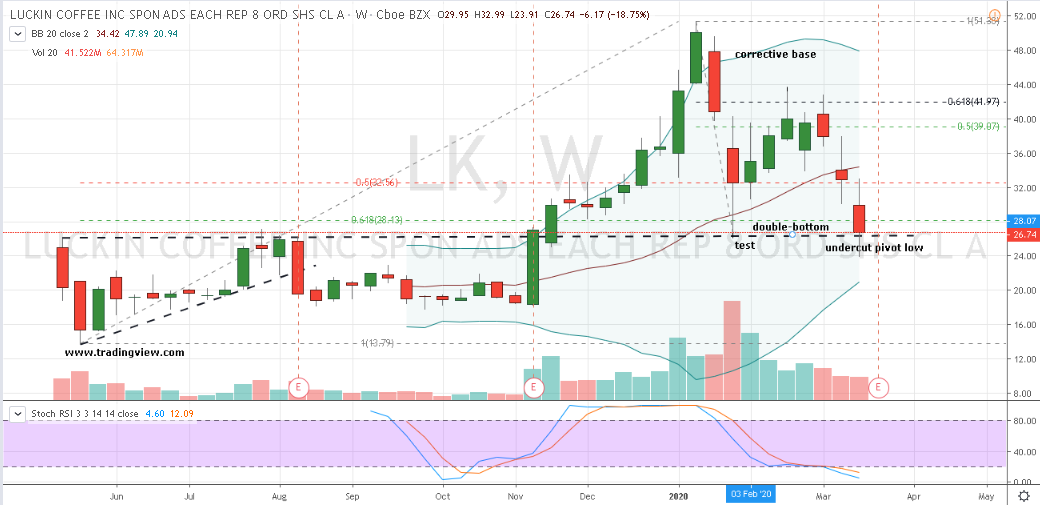

Luckin Coffee (LK)

Click to Enlarge

Luckin Coffee (NASDAQ:LK) is our next restaurant stock to buy. For investors wanting the next Starbucks (NASDAQ:SBUX) in their portfolio, the NASDAQ-listed and China-based mid-cap upstart is about as close as you’re going to get.

Prior to the coronavirus, the coffee purveyor had been growing like crazy overseas. And many investors were waking up to LK stock’s prospects, as shares of the recent IPO began to explode higher. However, the disease and ensuing store closures put a kibosh on that growth and investor enthusiasm in the near-term. But don’t make the mistake of turning your back on this restaurant stock.

Overall and longer-term, new coronavirus cases are dropping to nearly zero in China daily. And with a nicely-brewed, healthy double-bottom on the LK price chart emerging, this restaurant stock is well-positioned for bullish follow-through to higher prices.

Jack in the Box (JACK)

Click to Enlarge

Jack In The Box (NASDAQ:JACK) is the last of our restaurant stocks to buy. I’m not much for burgers these days, unless it’s a faux-meat patty from Beyond Meat (NASDAQ:BYND). But when I get the craving, Jack in the Box’s Sourdough Jack and curly seasoned fries are worth it. And right now, shares of JACK stock are worth biting into, as well.

Jack in the Box sports a measly market capitalization of just under $1.5 billion. Moreover, the fast-food chain has a solid franchisee model still open for business via storefront drive-thru’s or delivery channels from Uber (NYSE:UBER), Grubhub (NYSE:GRUB) and others. If you’ve got the munchies, 24/7 Jack in the Box is there.

Collectively, after JACK’s 73% grilling this past month and return towards the darkest days of the financial crisis, it’s time for this restaurant stock “to-go” into your portfolio.

The information offered is based upon Christopher Tyler’s observations and strictly intended for educational purposes only; the use of which is the responsibility of the individual. For additional market insights and related musings, follow Chris on Twitter @Options_CAT and StockTwits. Investment accounts under Christopher Tyler’s management currently own positions in Beyond Meat (BYND) and its derivatives, but no other securities mentioned in this article.