Shopify (NYSE:SHOP) was on a smooth uptrend in 2019. From $138.5 at the beginning of the year, Shopify stock surged by 196% to highs of $409.6.

Currently, the stock is lower by 26% and trades at $302. A 26% correction can just be on account of profit booking after a massive rally.

However, I believe that Shopify stock is likely to remain sideways to lower in the coming quarters. While I am bullish on business growth, I remain bearish on the stock for the foreseeable future.

Overall, it makes sense to remain on the sidelines as the stock might has run-up significantly ahead of fundamentals.

Cash Flow Not Coming Anytime Soon

If we leave aside high growth or early-stage companies, most of the valuation is on the basis of cash flows. No doubt, SHOP is still growing at a healthy pace, but robust cash flows are not coming anytime soon. This is for a company that has a current market capitalization of $35 billion.

For the first six months of 2019, SHOP reported a loss of $75 million at the operating level with cash flow from operations at $47 million. The operating cash flow is likely to remain volatile and I don’t see the business turning into a cash machine anytime soon.

The following points from the company’s presentation put things into perspective –

Expected spend of approximately $1 billion over next five years (consisting of expected cost to build and variable cost to operate). We expect incremental revenue to largely offset costs. Bulk of spend comes with scale and is success-based, bulk of net return expected beyond 2023.

Clearly, SHOP is still on an aggressive spending and expansion spree. The company’s cash flow is unlikely to be robust in the coming years. I don’t see that as a problem considering the business growth prospects. However, I do see the company’s valuation as an issue, and market sentiments seem to be gradually returning to sanity.

Sustained Growth and Shopify Stock

SHOP will continue to invest heavily in the next five years and that will impact profits at the operating level and the company’s cash flow. However, I believe that strong revenue growth will sustain. There are several factors that support my view.

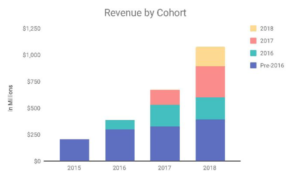

The chart below gives the company’s revenue by cohort. The interesting point to note is that revenue from pre-2016 cohort has been growing. The trend is similar for cohort in 2016 and 2017.

The company explains this growth in their 2018 annual report –

In 2018, revenue from the pre-2016 cohort accelerated its growth over 2017 as merchant retention improved, and the remaining merchants increased their GMV and adopted additional solutions provided through the Shopify platform.

Therefore, as businesses grow on the SHOP platform, they utilize higher subscription and additional services. This translates into higher revenue from the same client over a period of time.

The bottom line is that as the client base swells, cohort revenue will accelerate. At one point of time, investments will decline and the strong client base will continue to boost revenue. That’s when operating cash flows will surge. However, investors still need to wait for the next few years to witness that trend.

The second important point to note is that SHOP generated 55% FY18 revenue from the United States and 76% of revenue from top 4 countries. These include the U.S., UK, Canada and Australia. However, the company had 820,000 merchants from 175 countries as of FY18.

With rapid growth of eCommerce globally, there is huge impending potential for growth. During 2Q19, SHOP launched native language capabilities in more than 11 languages. With this, the company has Shopify Admin available in 18 languages.

This includes Chinese and Hindi. India and China are home to 2.5 billion people with rising living standards and high growth in the eCommerce industry. Clearly, there is a massive scope for scaling-up and Shopify is well-positioned to do that.

Final Thoughts on Shopify Stock

Shopify has a robust cash buffer and the recent equity offering will add to the cash position. Therefore, there are no concerns related to aggressive investment for growth and technology.

However, the stock seems overvalued considering the fact that the company expects the “bulk” of net returns beyond 2023.

For 2019, the company expects GAAP operating loss in the range of $145 to $155 million. Losses can potentially continue in 2020 as high investments continue.

After the massive rally, I expect the current correction to sustain. Another 15% to 20% downside from current levels will not be surprising. However, it would make sense to accumulate Shopify stock in the range of $250 to $270.

As of this writing, Faisal Humayun did not hold a position in any of the aforementioned securities.