Right now, the conventional wisdom is that this is a good time to look at aerospace/defense stocks. And if you look at a chart, there’s good evidence for that.

People tend to race into defense stocks whenever there’s turmoil overseas. While it’s always troubling on a personal (and political) level, there is a silver lining economically. Major employers here in the U.S. in this space, like Boeing (NYSE:BA) and United Technologies (NYSE:UTX), tend to see nice share-price appreciation.

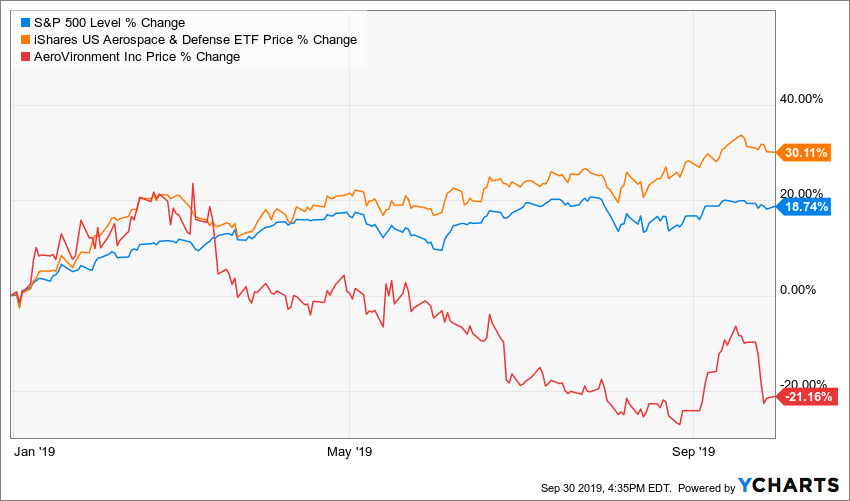

That’s certainly been the case now. Below you can see it reflected in the iShares U.S. Aerospace & Defense ETF (BATS:ITA). The group has begun to strongly outperform the broad market on the heels of the recent attack on Saudi oil fields, and continuing tension with Iran.

That being said, one of the best pieces of investment advice I could ever give you is this: Not all stocks in a sector are created equal. And this chart is a good example of that… as stocks like AeroVironment (NASDAQ:AVAV) are, ultimately, not participating.

At times like these when defense stocks are in favor, AVAV, a California-based maker of unmanned aerial vehicles (UAVs), more commonly known as drones, is normally something I’d be looking at for my model portfolios for newsletters like Growth Investor.

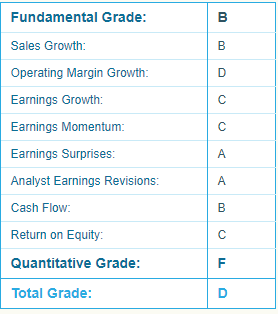

Well…the Report Card from my Portfolio Grader (below) shows you why we are staying away:

The picture for AVAV is not entirely bad; the company has a history of good sales growth and positive earnings surprises, as well as upward revisions in Wall Street analyst’s forecasts for the company, and cash flow.

However, other factors inspire serious concerns. Earnings Growth and Earnings Momentum could be a lot better; Operating Margin Growth is downright ugly.

Worst of all, AVAV currently scores an “F” for its Quantitative Grade. This suggests that big money on Wall Street is fleeing the stock. That is, in fact, the biggest factor in any growth investment’s long-term success – contributing to AVAV being a D-rated “Sell” at this time.

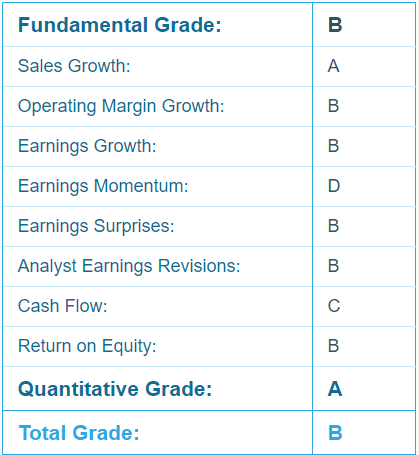

Meanwhile…another lesser known aerospace/defense play, Woodward (NASDAQ:WWD), is looking a lot more appealing.

Take a look at my Report Card on WWD:

While Earnings Momentum leaves something to be desired, overall Woodward has strong fundamentals.

In early August, WWD crushed analysts’ earnings and sales estimates for its third quarter in fiscal year 2019. During the third quarter, sales increased 28% year-over-year to $752 million. That topped forecasts for sales of $694.08 million.

Third-quarter earnings per share jumped 32.5% year-over-year to $1.02, up from $0.77 per share in the same quarter a year ago. Adjusted earnings per share rose 16.1% year-over-year to $1.30. So, since analysts had only expected $1.16, the company posted a 12.1% earnings surprise.

Looking ahead, Woodward expects fiscal year 2019 sales of $2.9 billion, with aerospace sales rising 19% year-over-year and industrial sales jumping 35% year-over-year. Adjusted earnings per share are forecast to be between $4.70 and $4.80. That represents 24.5% annual sales growth and 22.1% to 24.7% annual earnings growth.

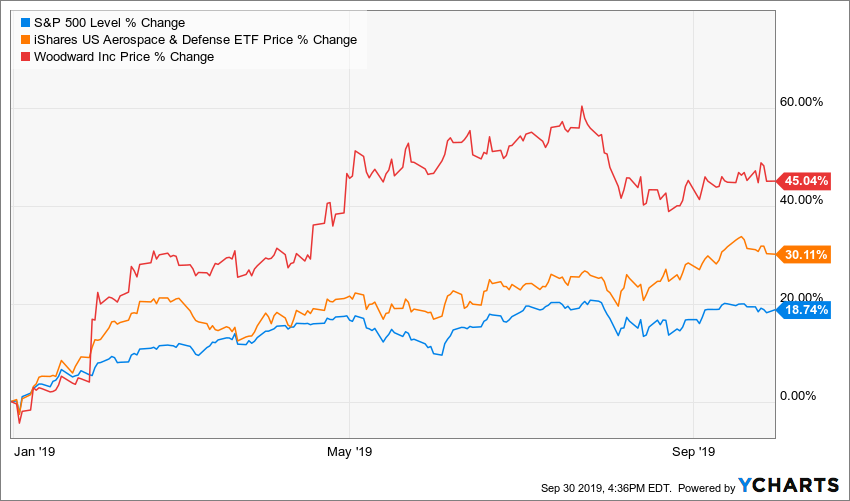

No wonder WWD stock is far outpacing the broad market and the sector, as we see here:

So now we see the context for not only the Fundamental Grade of “B,” but the Quantitative Grade of “A.” Major institutional cash is clearly finding a home in WWD stock, and that’s the kind of investment we should be looking for in this (and any) sector.

Timing is Everything

Even with some of the highest quality stocks in a sector, as is true of WWD stock for aerospace/defense, the most important thing is to get the timing right.

If you’re a growth investor – and I certainly am; I’ve made my career this way – then you’ve got to look for elite growth statistics like Woodward’s. I’m also recommending several other aerospace/defense plays for subscribers right now; in Growth Investor, we’ve got a healthy weighting in several OTHER sectors as well.

We’re seeing no need to react to headlines in making our investment decisions, however. We focus on fundamentals and buying pressure. Those two factors alone are responsible for much of your long-term success with growth stocks.

There’s another factor I’ve got my eye on — and I’m hardly alone in that, especially these days. I’m talking about dividend investing.

These days, the global bond market is just going haywire: We’ve got falling and even negative yields overseas. But as investors retreat to U.S. Treasurys it’s causing bizarre effects here, too. Just look at what happened this summer, when the two-year Treasury actually began to yield MORE than the 10-year Treasury. And even the 30-year Treasury can’t be relied upon for good yield anymore. In August, its yield dropped below 2% for the first time ever.

So — whether you’re managing big institutional cash, or your own portfolio — you’ll also want to look at the Money Magnets.

Not only did these stocks earn an “A” in my Portfolio Grader, thanks to strong buying pressure and great fundamentals …

The stocks also earn an “A” in my Dividend Grader. These stocks are able to pay great yields — and have the strong business model to back it up.

All in all, I’ve got 27 strong dividend growth stocks for you now, and one more coming, in Growth Investor. These stocks are poised to do well as we continue to see international capital flow to the U.S. markets. Click here to see how I found these stocks, and how you can get great performance out of YOUR portfolio — come what may.

Louis Navellier had an unconventional start, as a grad student who accidentally built a market-beating stock system — with returns rivaling even Warren Buffett. In his latest feat, Louis discovered the “Master Key” to profiting from the biggest tech revolution of this (or any) generation. Louis Navellier may hold some of the aforementioned securities in one or more of his newsletters.