Canopy Growth (NYSE:CGC) is a popular stock for cannabis investors due to the company’s high valuation. But the company’s growth story is much less compelling than it was a year ago. CGC stock is currently down 51% after a series of missteps.

I’ll admit to being a skeptic when it comes to most of the cannabis companies that are currently on the market. And here are four reasons why I don’t think the narrative will improve for CGC stock.

CGC is still not profitable

In terms of valuation, Canopy Growth is considered the world’s largest cannabis company, clocking in at yesterday’s close at $8.8 billion. And thanks to a $4 billion equity investment from Constellation Brands (NYSE:STZ), the company has access to a considerable amount of cash. Yet CGC remains unprofitable, mostly because it continues to burn through money at such a rapid pace.

The company has been on a spending spree for the better part of the last two years. Canopy Growth continues to move into new markets and construct new production facilities. There are advantages to this but it puts the company nowhere near profitability.

Tenuous Leadership

In July, the board publicly ousted CEO Bruce Linton after a wide earnings miss. Currently, CEO Mark Zekulin is leading the company but this is a temporary position and Zekulin plans to step down eventually. The board is currently looking for Linton’s replacement.

This tenuous leadership means CGC doesn’t have a real visionary guiding the company. The lack of leadership could be a contributor to many of the company’s recent challenges.

Strict Governance in the U.S. and Canada

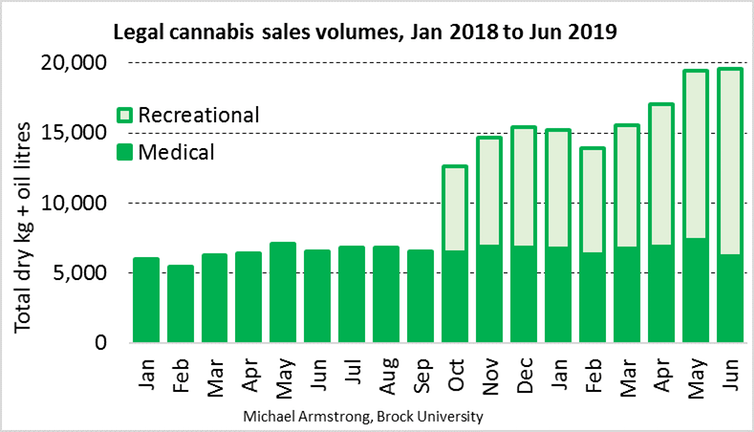

The cannabis industry is dealing with strict regulations across the U.S. and Canada. Health Canada is the agency responsible for overseeing the cannabis industry in Canada. The agency currently has 800 sales and production licenses to review and it can take up to a year for a company to gain regulatory approval. The chart below illustrates what’s happened in the first nine months of legal cannabis in Canada.

Canadian academic Michael Armstrong’s research (chart) showed that one reason legal sales haven’t done better is a lack of retailers in some regions. British Columbia and Ontario were especially slow to open stores. Chalk that up to the licensing backlog.

These regulatory issues are happening across the U.S. as well. Many states are slow to approve dispensary licenses. For instance, Missouri received more than 2,100 applications for dispensary licenses but so far, only 109 have been approved.

Uncertainty Within the Cannabis Industry

The ongoing media narrative is that cannabis stocks are the next real growth story. The industry should take off in the next decade, though these estimates vary depending on where you find them. According to Forbes, legal spending on cannabis should reach $57 billion by 2027.

But leading companies like Aurora Cannabis (NYSE:ACB), Tilray (NASDAQ:TLRY), and CannTrust Holdings (NYSE:CTST) have seen their shares plummet over the past six months. Most of these companies produce more cannabis than they can sell. And CannTrust had its cannabis licenses suspended by Health Canada after recent inspections of several of its production facilities.

There’s no doubt that the marijuana industry provides plenty of opportunities in the coming years. It just seems unlikely that the cannabis companies currently on the market, like CGC, will be the ones to take the industry to the next level.

As of this writing, Jamie Johnson did not hold a position in any of the aforementioned securities.