The labor market and the broader economy are both better than they look on the surface, and in fact have been mostly defying the continual patter of recession expectations.

By multiple measures, the U.S. is staying ahead of the global slowdown, the trade war with China and the bond market’s implication that the decade-long recovery after the financial crisis is coming to a close. Though the major Wall Street averages wobbled around breakeven Tuesday, stocks are back near record highs as investors shrug off the wave of fear.

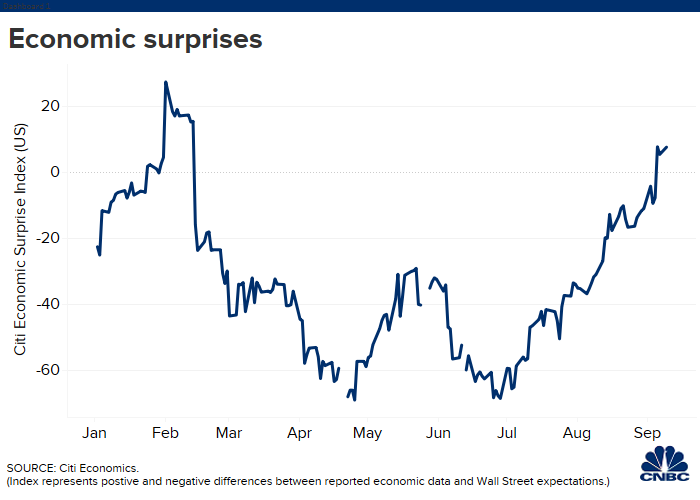

One gauge in particular shows how much the economy has defied downbeat forecasts.

The Citi Economic Surprise Index, after nearing its lowest level in two years in June, this week was at its highest point since February. The index looks at actual economic readings against consensus forecasts, so it will rise when expectations are too low and fall when optimism runs too strong. The latest move, then, can be seen as a recalibration of Wall Street’s overriding pessimism.

“The indicators have been surprising to the upside rather than the downside, which is a good development,” said Ed Yardeni, founder of Yardeni Research and a follower of the Citi gauge. “It kind of raises the question of why the Fed is even considering lowering interest rates at the next meeting.”

Markets widely expect the central bank to cut its benchmark overnight lending rate by a quarter percentage point next week, likely citing low inflation, tariff uncertainty and weakness in Europe and China.

However, the news from home might limit the Fed’s desire to keep cutting.

Friday’s nonfarm payrolls report might have provided headline fodder for those, like President Donald Trump, who believe the Fed should be significantly looser with policy. But a closer look at the number chose a far more resilient labor market.

The total job growth came in at 130,000, which missed the meager expectations of 150,000 and was just 96,000 when eliminating the gains in government payrolls, thanks mostly to Census hiring.

But Goldman Sachs chief economist Jan Hatzius pointed out in a note that the numbers “likely understate the trend because of the well-known seasonal adjustment distortions in the preliminary August release.”

Indeed, August is a notoriously noisy payrolls month, often subject to substantial revisions. In 2018, the initial count of 201,000 ultimately ended up at 282,000, 2017’s started at 156,000 and ended at 187,000, and 2011 was notorious for registering a zero on first release that ultimately came in at 122,000.

In fact, Goldman sees not only stronger payroll growth but also even higher pressure on wages than the 3.2% annualized that the Labor Department reported. Hatzius said the firm’s various wage trackers put earnings growth at 3.4%, which would be the best level of a recovery that began in mid-2009.

The firm sees rate cuts in September and October as likely, but also projects that “the environment will become less supportive for further” moves as inflation moves up and economic growth settles in around 1.75% annually.

Quitting with confidence

More signs of a strong labor market came out Tuesday.

The Job Openings and Labor Turnover Survey for July — the reading runs a month behind nonfarm payrolls — showed there are still 1.17 million more job openings than available workers. Hires outnumbered separations by 194,000 and the quits level, which measures employees who voluntarily left their jobs and is considered a yardstick for worker confidence, rose by 130,000, up 0.1 percentage point to 2.4%.

Finally, Tuesday’s National Federation of Independent Business Survey, which polls small businesses, found that 57% of all respondents reported that finding qualified workers remains their biggest staffing challenge.

“Just about every labor market indicator that’s come out before and after the weak payroll number on Friday suggests the labor market is doing great,” Yardeni said. “There’s no recession.”

Still, worry remains that contraction signs in manufacturing gauges, a still-weak profits outlook and the yield curve inversion in the bond market are all foretelling a recession over the next year or so.

David Rosenberg, chief economist and strategist at Gluskin Sheff, said in his daily note Tuesday that expectation for third-quarter GDP of around 1.5% is “otherwise known as ‘stall speed’ and in the old days, GDP growth estimates would have been generating significant recession chatter as opposed to all the ‘focus on the underlying fundamentals’ talk.”