Traders and financial professionals work at the opening bell on the floor of the New York Stock Exchange (NYSE) on August 6, 2019.

Drew Angerer | Getty Images

Corporate America’s aggressive program of buying back stock slowed in the second quarter.

Data provided by Standard & Poor’s indicates that corporate buybacks totaled $166 billion in the second quarter, a 13% drop from the $190.6 billion a year earlier.

Is Wall Street’s eagerness to buy back its own stock cooling?

Howard Silverblatt, who tracks buybacks and other corporate data for Standard and Poor’s Dow Jones Indices, says the drop needs to be understood against the huge increase in 2018: “You have to take 2018 as an outlier. There was a big boost there” due to the tax cuts, he said.

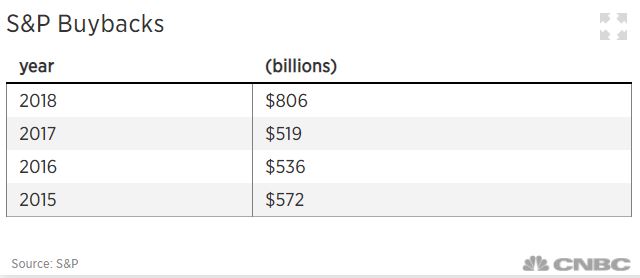

Silverblatt notes that, thanks to tax cuts stuffing corporate America’s coffers with fresh cash, 2018’s buyback total of $806 billion was far and away the biggest year ever, dwarfing the record $572 billion set in 2015 by nearly 40 percent.

Given the blip from the tax cut, it’s little wonder that 2019 is not quite as strong.

It’s long been believed that corporate America’s aggressive buyback program has been a key contributor to the market’s advance this decade. In April, Ed Clissold, chief U.S. strategist at Ned Davis Research, told clients, “Without focusing too much on numbers, we can say that the S&P 500 index would probably be lower today if not for buybacks versus other uses of cash. “

How much depends on what exactly the money was used for. The firm looked at the S&P 500′s performance between the first quarter of 2011 and the first three months of 2019. The broad market was up 125% in that time. Clissold estimates that had the money simply been held as cash, the S&P would be 5% lower than it is now. If companies used the money instead to pay dividends, the S&P would be 10% lower. If the money was reinvested into their businesses, Clissold estimates the S&P would be just 2% lower.

Bottom line: Buybacks have contributed to the market’s advance, though perhaps not as much as some believe.

“There’s clearly other buyers out there helping the rally along,” Silverblatt said. “Do buybacks beat out earnings and other factors as the main mover of stocks? No, but it is one of the factors that have to be taken into account.”

What is clear is that the high level of buybacks indicates that corporate America still believes buybacks provide a superior return to shareholders. Silverblatt noted that cash flows remain strong, and financing is cheap and available — all of which helps the buyback story.

What’s not yet clear is what the “new normal” level will be: Do we go back to the mid-$500 million level of the last several years, or do we stay up at a permanently higher level?

Based on buybacks in the first half, Silverblatt estimates that 2019 buybacks could total $740 billion, an 8% drop from 2018’s torrid pace but still the second best year on record.

That is nothing to sneeze at: “You won the lottery last year, you can’t be too mad you didn’t win the lottery again next year,” Silverblatt said.